The Top MGAs in Canada | 5-Star

Brokers on MGAs

Jump to winners | Jump to methodology

Staying power: the MGA advantage

The top MGAs in Canada are winning on performance. In a market where broker reliance has levelled into consistent patterns, Insurance Business Canada’s 2025 Brokers on MGAs survey highlights the organizations that distinguish themselves through responsiveness, technical expertise, and ability to place risks that direct markets will not touch. Their strength lies less in market share and more in how they deliver speed, sound governance, and specialized capacity that brokers value most.

As executive director of the Canadian Association of Managing General Agents (CAMGA), Steve Masnyk, put it, “A valuable MGA to brokers is one that is an expert in a certain niche product or class, in a certain region of the country, and one whose service levels exceed what carriers are offering today. It’s a trusted partnership between the broker and the underwriter.”

IBC’s 2023–25 survey data show a channel defined by consistency. Broker reliance on MGAs has neither expanded nor declined but instead settled into a dependable mid-tier role. MGAs remain the go-to option for specialty placements and flexible capacity, while the bulk of broker business continues to flow through direct markets. IBC’s survey confirms a pattern of steady use, where brokers lean on MGAs for certain classes, but not as their dominant distribution channel. Or, as Masnyk says, “There is no such thing as a bad risk; there are only badly priced risks.”

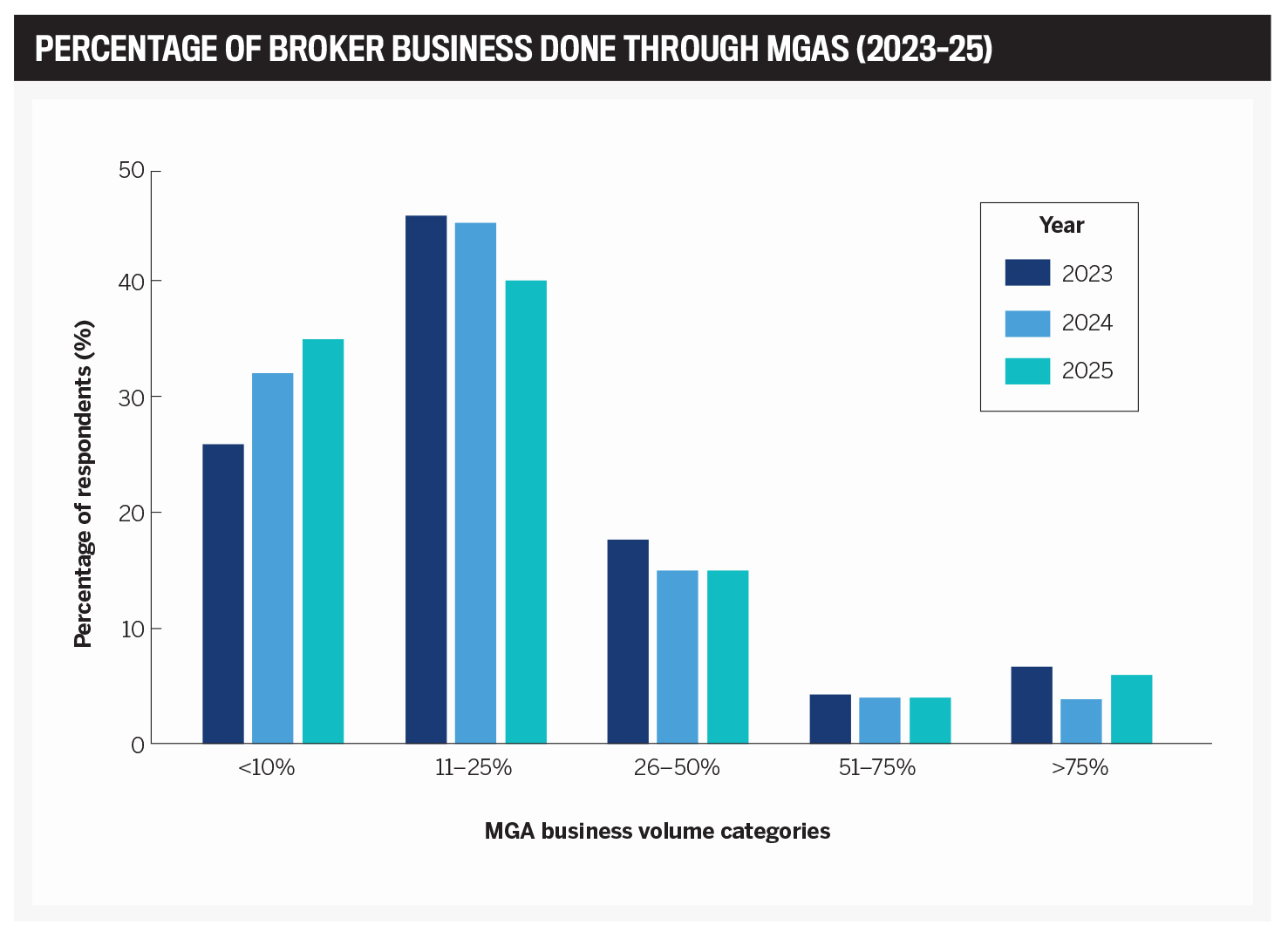

Broker reliance on MGAs stays consistent

Takeaways:

-

MGAs hold a stable, mid-tier role in distribution – they are essential but not dominant.

-

A total of 40–46 percent of brokers place 11–25 percent of their book through MGAs.

-

Low-volume users (<10 percent) rose to 35 percent in 2025, showing that more brokers engage with MGAs lightly.

-

Heavy reliance (>50 percent of book) holds at 8–11 percent.

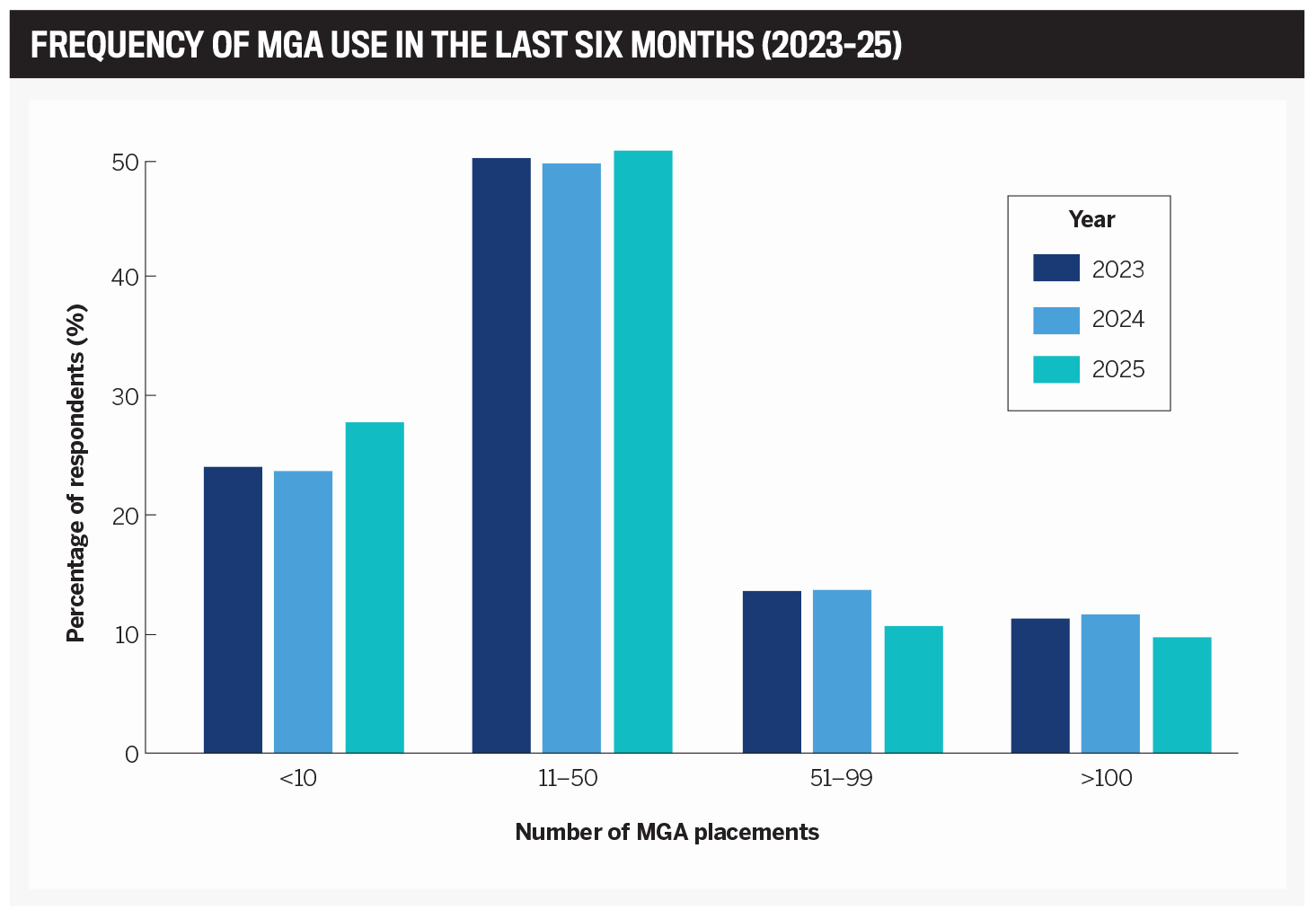

Broker use of MGAs holds firm as a placement channel

Takeaways:

-

MGAs remain embedded in broker workflows, valued for specialty risks but not expanding share.

-

About half of brokers place 11–50 risks through MGAs every six months.

-

Low-frequency users (<10 placements) account for just over one-quarter of brokers, steady since 2023.

-

High-frequency users (51+) make up about one-quarter of brokers, showing consistent heavy reliance.

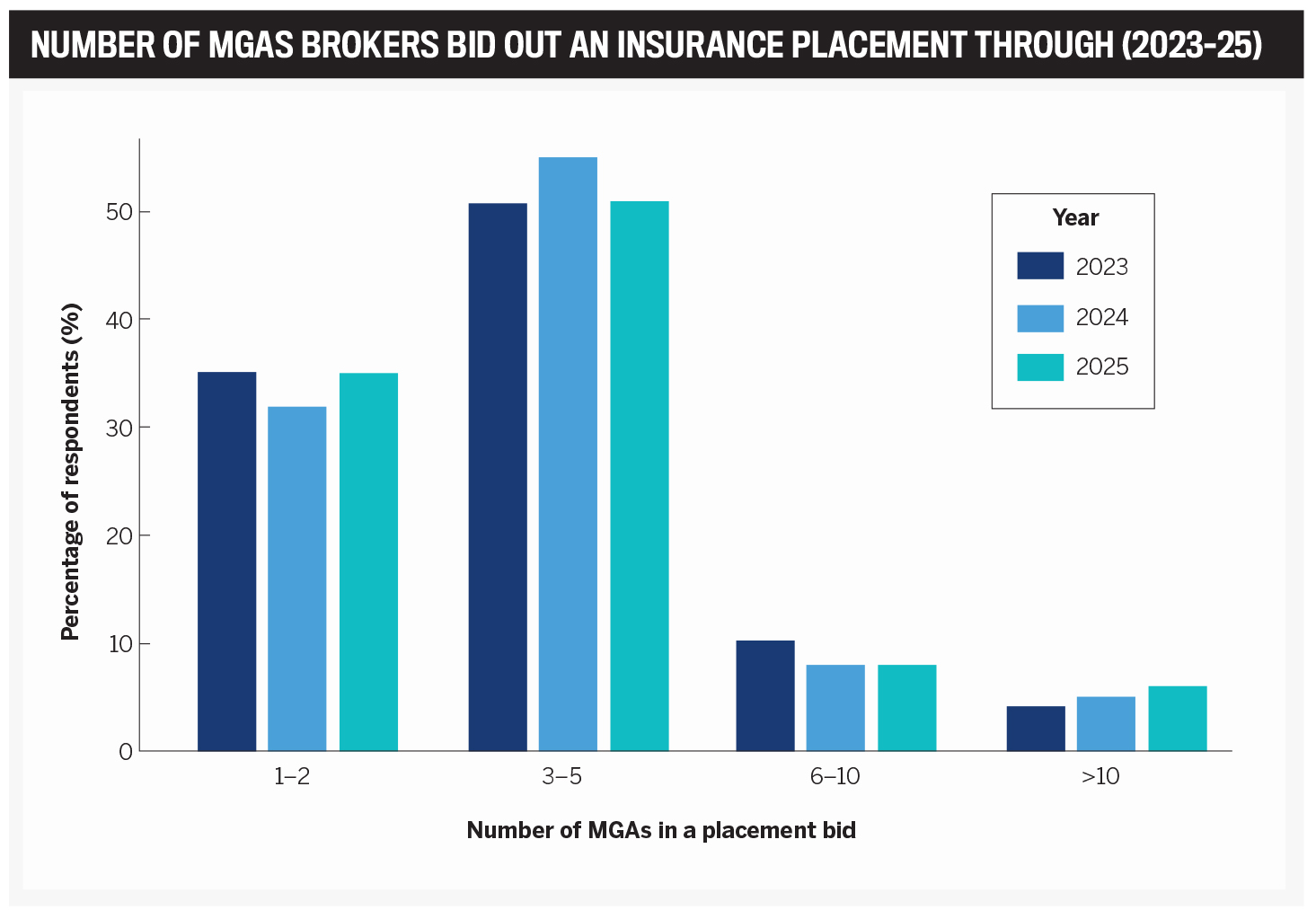

Broker bidding practices remain steady

Takeaways:

-

Most brokers balance competition with efficiency by bidding placements to three to five MGAs.

-

Half of brokers use panels of three to five MGAs, a norm that has held over three years.

-

One in three places business with just one to two MGAs, favouring trusted relationships over broader competition.

-

Larger panels of six or more remain limited at 12–14 percent of brokers.

To identify the top MGAs in Canada’s wholesale distribution channel, IBC surveyed brokers nationwide, asking them to rate the performance of their partners across 10 key metrics, from responsiveness and technical expertise to placing niche risks.

Responses were scored, and MGAs earning an average score of 4.0 or higher (on a scale from 1, meaning poor, to 5, meaning excellent) in at least one category received a 5-Star designation. Those scoring 4.0 or higher across all categories achieved All-Star status.

Brokers also ranked their top three MGAs across 20 major insurance lines and highlighted the best MGA products. Gold, silver, and bronze medals went to the top three in each line, while the three insurance products with the most broker votes earned the Brokers’ Pick medal.

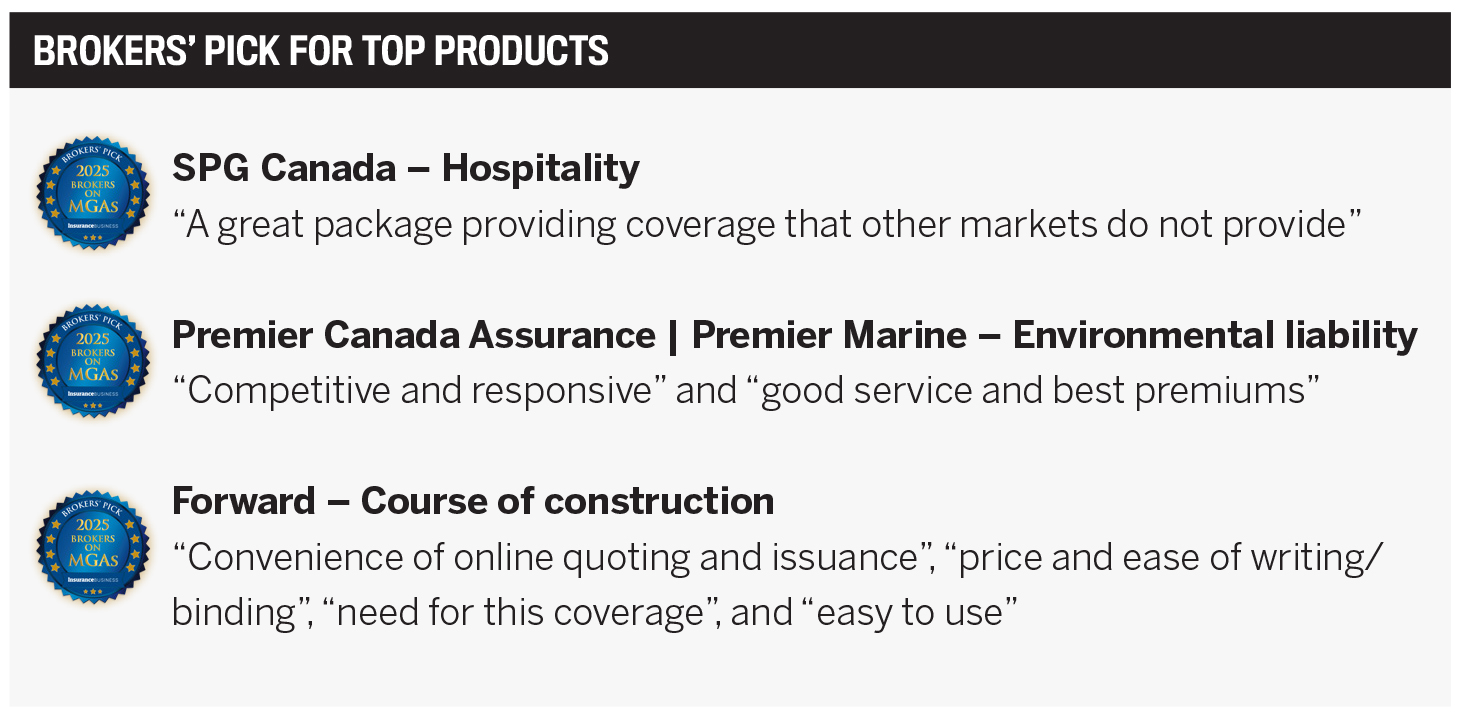

- Forward – Course of construction

- “Convenience of online quoting and issuance”, “price and ease of writing/binding”, “need for this coverage”, and “easy to use”

- “Convenience of online quoting and issuance”, “price and ease of writing/binding”, “need for this coverage”, and “easy to use”

- SPG Canada – Hospitality

- “A great package providing coverage that other markets do not provide”

- “A great package providing coverage that other markets do not provide”

- Premier – Environmental liability

- “Competitive and responsive” and “good service and best premiums”

- “Competitive and responsive” and “good service and best premiums”

Canada’s MGAs remain entrenched and adaptive

The MGA sector has become a fixture of the market. It now manages billions in premium, giving brokers access to coverage in areas where direct markets fall short. Carriers are leaning in, too, expanding delegated capacity even as commercial rates slide.

Regulators, meanwhile, are tightening their oversight, while brokers continue to use MGAs in steady, mid-tier volumes. What emerges is a channel that is firmly established, strategically important, and adjusting to the combined pull of market forces and regulatory demands.

Scale and footprint

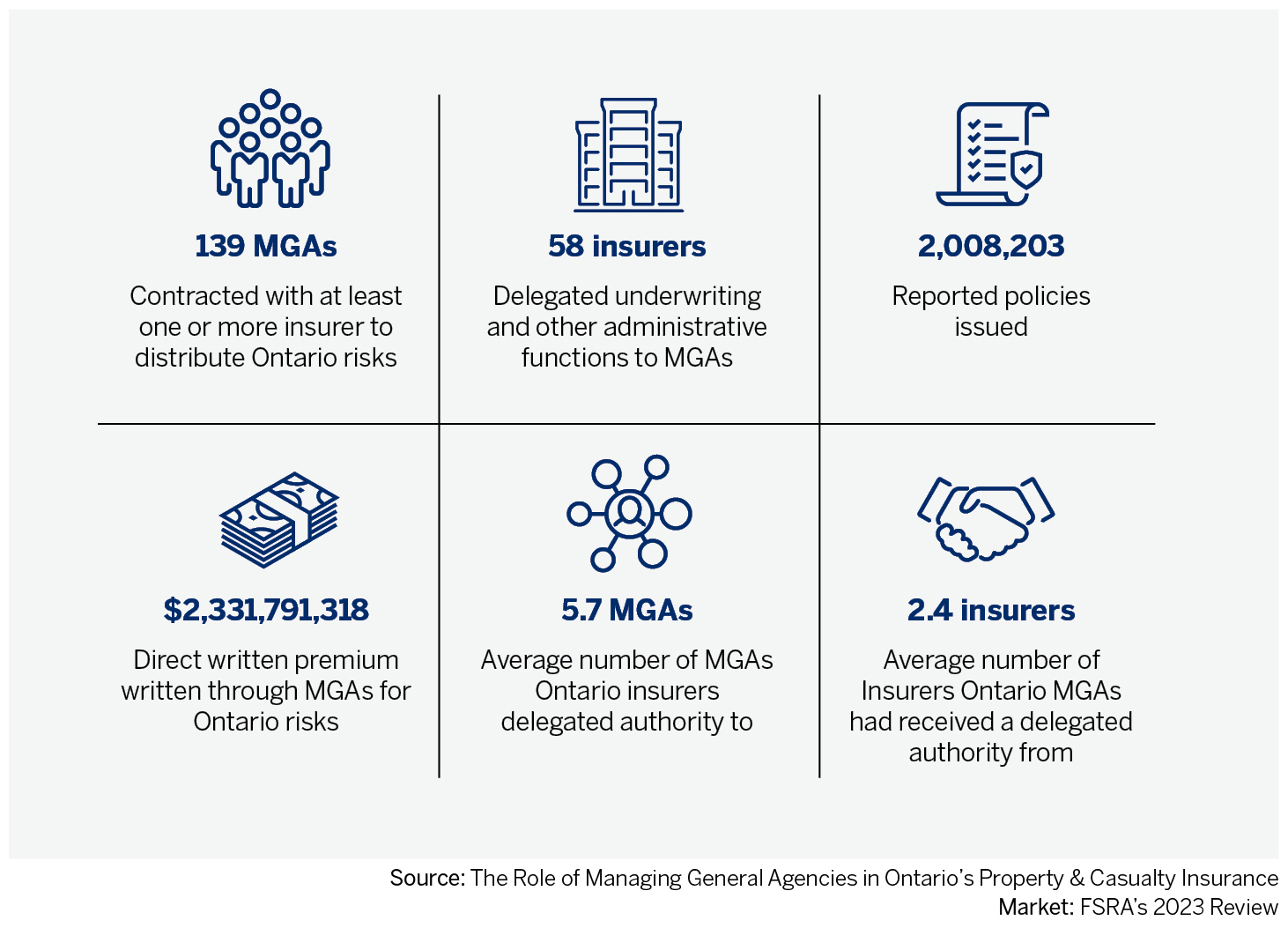

The most recent Financial Services Regulatory Authority of Ontario (FSRA) MGA market review, published in 2024 and based on 2023 data, quantified Ontario’s MGA footprint alone at $2.33 billion in direct written premium. That represents 6 percent of the province’s total P&C market. Total P&C DWP was pegged at $38.6 billion that same year.

FSRA reported 58 of 218 licensed insurers were using MGAs, with 139 active MGA-insurer relationships in place. Market concentration is evident, as one dozen MGAs accounted for about half the total volume.

This review now anchors FSRA’s broader Property and Casualty Insurance Market Conduct Supervision Strategic Plan, also released in 2025, which extends the regulator’s tools to thematic reviews, examinations, and oversight of insurers’ MGA arrangements.

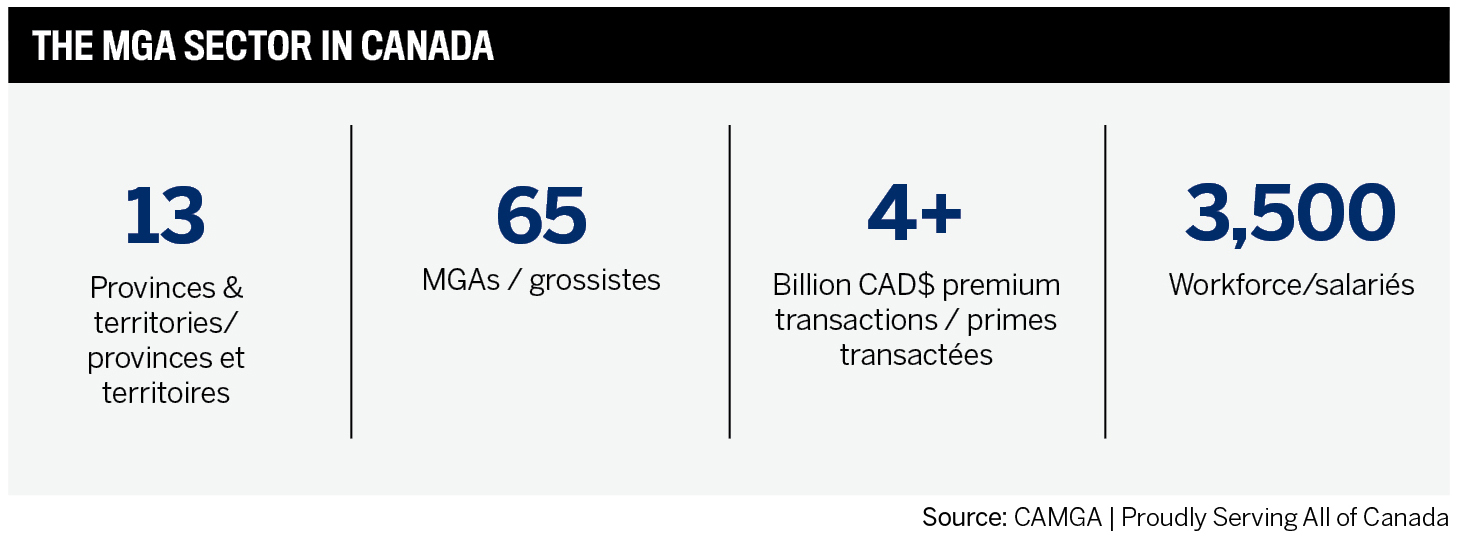

There is no single national MGA DWP tally, but industry sources place the number of MGA firms in Canada between 80 and 100, with the CAMGA reporting 65 members and describing that as about 80 percent of the country’s MGA population.

Market conditions and demand signals

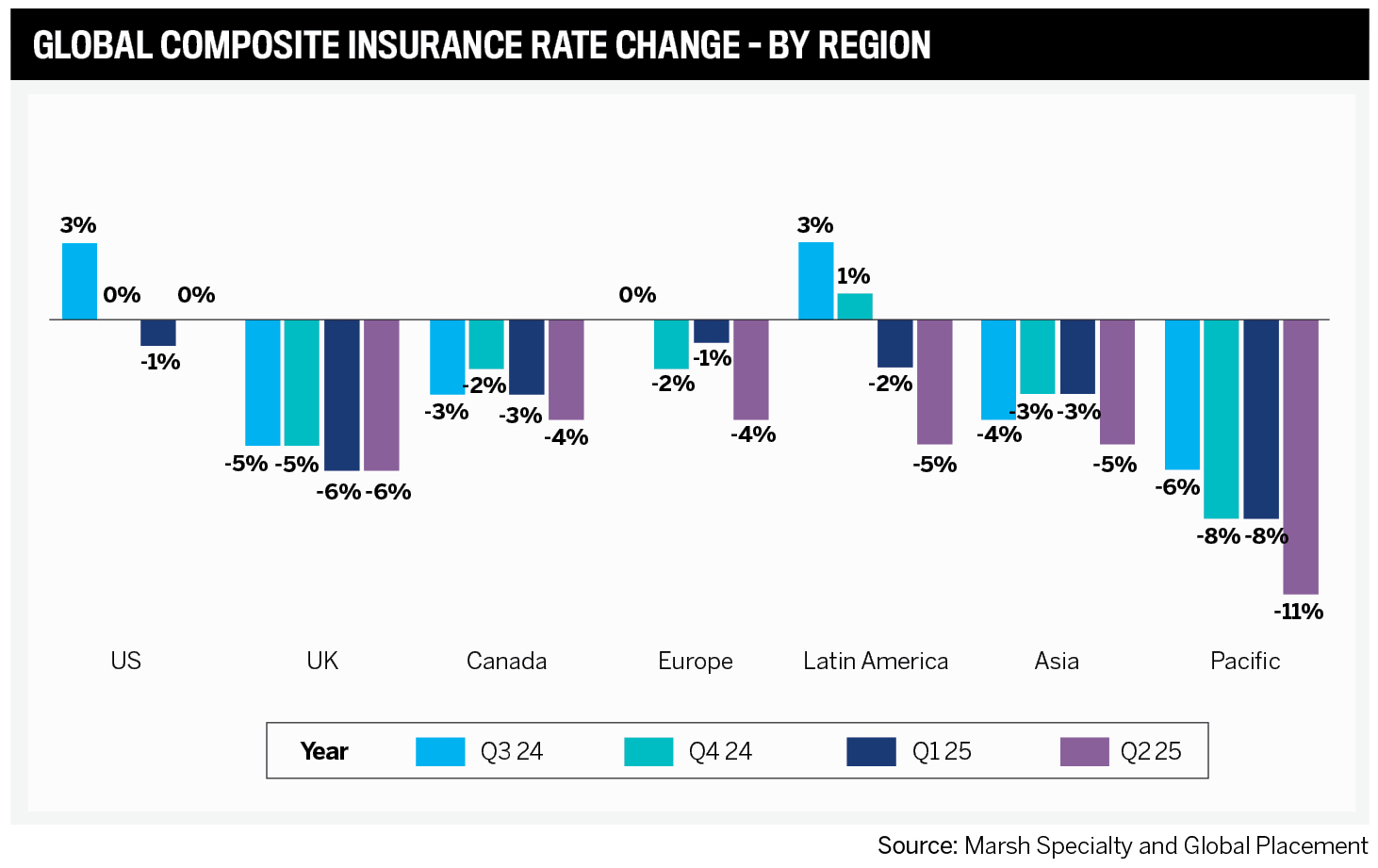

Rate momentum favours buyers. Marsh reports a 4 percent decline in global commercial insurance rates in Q2 2025, with Canada following the same downward trend for a sixth consecutive quarter, reinforcing competitive tension that often pushes brokers toward MGA solutions for speed, niche capacity, and service.

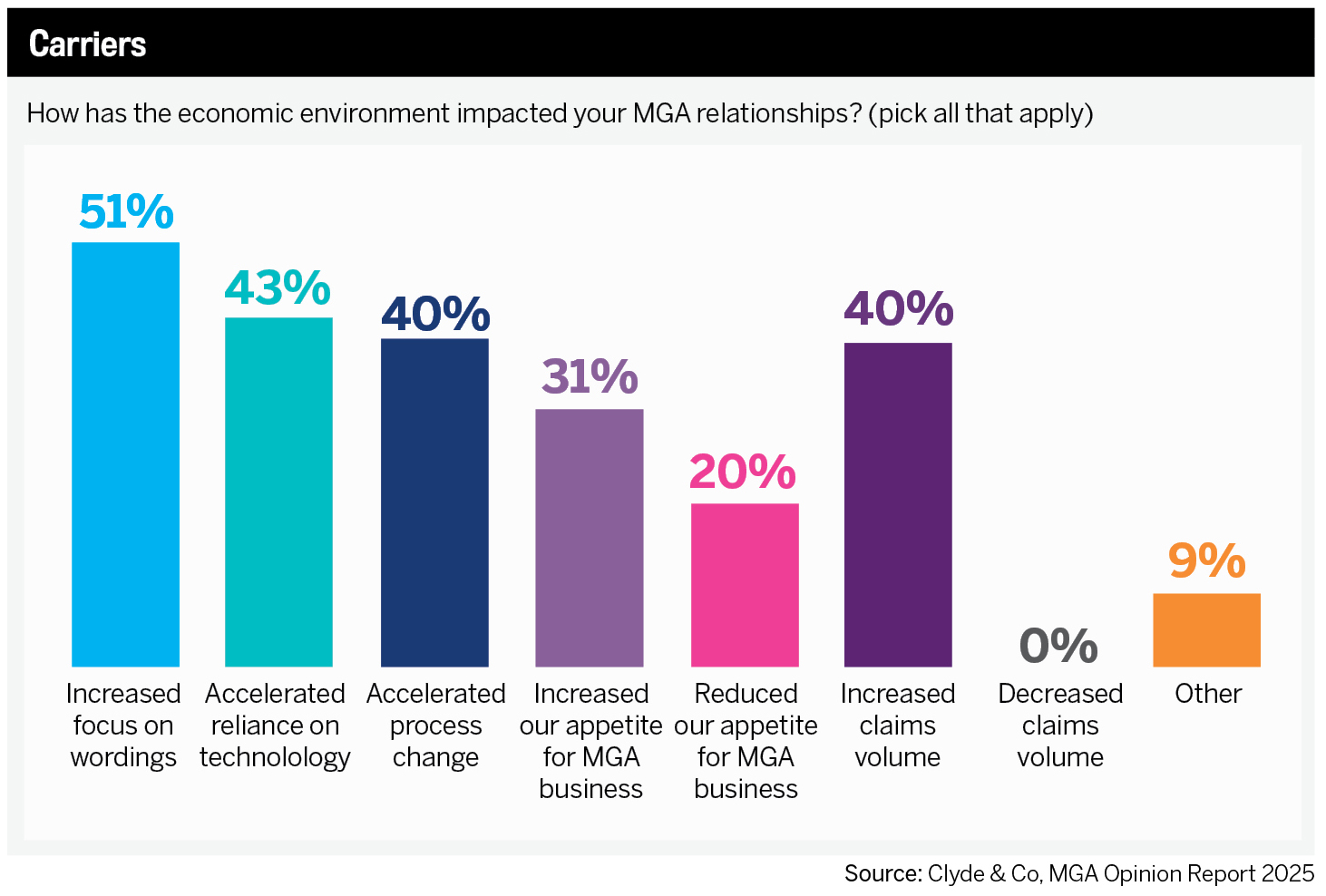

Carrier capacity and strategic posture

Carrier appetite for the model remains favourable. Clyde & Co’s MGA Opinion Report 2025 finds 57 percent of carriers expect to increase MGA capacity over the next two years, and 46 percent already did so in the past 12 months.

The same research flags pain points to watch:

-

A total of 77 percent of MGAs and 91 percent of carriers say claims process performance needs improvement.

-

Regulation is the top barrier to growth cited by both sides.

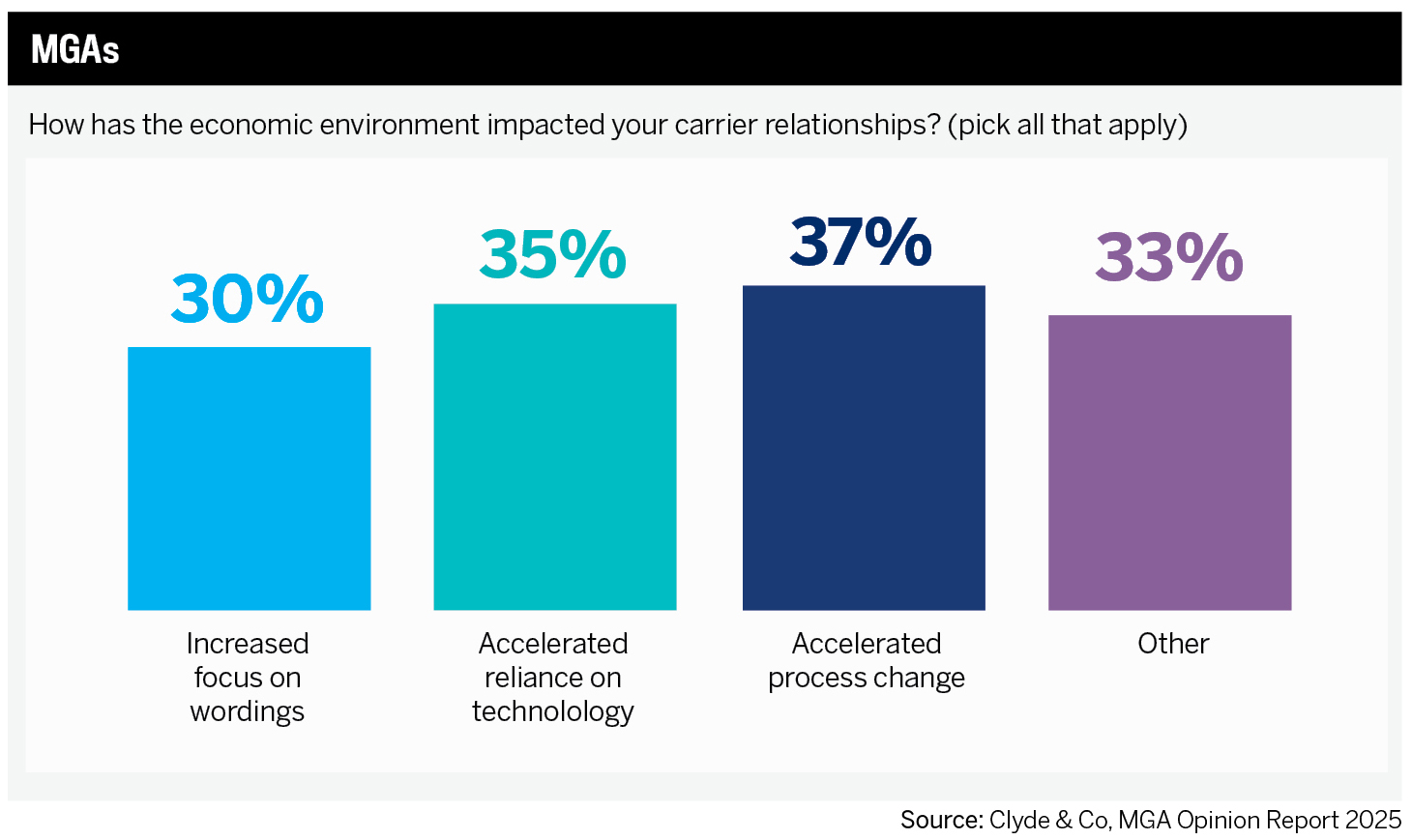

Rising costs, softer rates, and economic uncertainty are squeezing both MGAs and carriers. Even so, the sector is moving, not stalling. More than half of MGAs (54 percent) say today’s conditions will hurt their business, and 69 percent of carriers agree. But instead of retreating, the data points to a market adjusting and reshaping itself.

CAMGA’s Masnyk notes that product knowledge is what will make or break an MGA. “An underwriter needs to fully understand the exposures associated with a risk thoroughly, be knowledgeable about the types of claims associated with that risk, and be able to accurately price that risk, taking those factors into account,” he explains.

Regulatory trajectory

Oversight is tightening. FSRA released its Property and Casualty Insurance Market Conduct Supervision Strategic Plan in June 2025, formalizing a framework that includes risk assessments, thematic reviews, inquiries, and examinations.

FSRA’s earlier review of MGAs mapped their presence in Ontario and is now guiding more focused supervision, including checks on how insurers oversee their MGA partnerships. Senior leaders should expect more evidence-driven inquiries and higher expectations on governance, outsourcing controls, and data.

However, MGAs remain defined by their ability to enter underserved markets. “The most successful MGAs are those who enter a space where there is a lack of choice and providers, fill a gap in the market with expert underwriting, and meet the needs of that market, which other players either refuse or are unable to service,” says Masnyk.

Broker usage trends

IBC’s 2023–25 broker surveys show consistent use of MGAs:

-

mid-tier reliance is common

-

heavy reliance is contained

-

bidding panels remain concentrated around three to five MGAs

The role is entrenched for specialty and flexible placements, even as the bulk of the book stays with direct markets.

What it means for IBC’s 5-Star and All-Star MGAs

-

Operational discipline: As FSRA’s supervisory framework takes hold, MGAs that deliver strong internal controls, such as clear separation of duties, audit-ready oversight, and effective risk monitoring, will encounter fewer obstacles with carriers and regulators.

-

Claims and service: The claims interface remains the model’s weak point. MGAs that streamline handoffs, speed resolution timelines, and improve report clarity can leverage this as a point of difference in today’s market.

-

Capacity management: With commercial rates softening, declining 4 percent in Q2 2025, and carriers increasing capacity for specialty, financial, and property lines, MGAs that can move quickly on niche capacity while safeguarding underwriting rigour gain a tangible edge.

-

Data and transparency: Regulators are stepping up oversight of delegated authority arrangements, and carriers are demanding more consistent, timely data. Expect sharper scrutiny of how risks and premiums are reported and whether MGA information gives insurers the tools to meet their own compliance obligations.

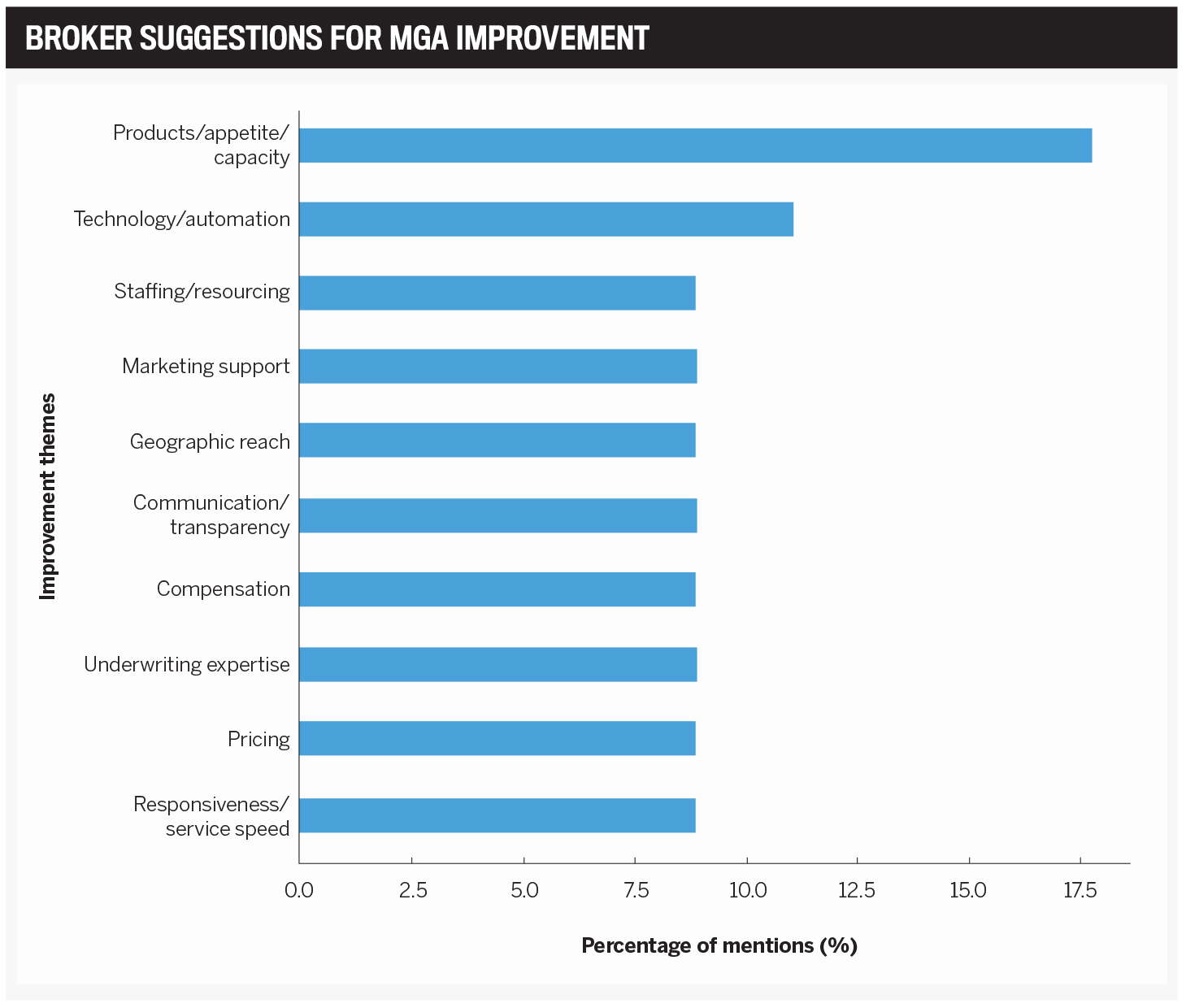

Broker suggestions for how MGAs can improve

Takeaways:

-

Broaden appetite and add capacity in niche markets.

-

Invest in technology that supports portal quoting and automation.

-

Commit to faster and more reliable turnaround times.

Broker feedback on how MGAs could improve shows a clear hierarchy of priorities. At the top of the list is the call for broader products and capacity. Brokers want MGAs to:

-

expand appetite

-

add coverages

-

fill the gaps left by direct markets

This demand runs across niches such as older renovated homes, hospitality with higher liquor receipts, mobile homes, and special events.

Masnyk remarks that Canada’s MGAs are growing simply because there are major gaps in the availability of products across the commercial space, and they fill these voids with expertise in underwriting and exceptional service levels. “It’s a pretty simple formula: provide an expertly underwritten product that is lacking and serve your brokers with the best service in the industry,” he adds.

Technology is the second major theme. Brokers are looking for:

-

more portal-ready products

-

straight-through quoting for simple risks

-

smoother renewal processes

The appetite for automation is tied directly to efficiency. Respondents want quick access for straightforward risks while still being able to rely on underwriters for complex cases.

Speedy service rounds out the top three. Delays in quotes and inconsistent follow-up are the most common frustrations. Brokers are asking for:

-

clear SLAs

-

faster callbacks

-

more reliable response systems that reduce bottlenecks

Why brokers keep coming back to

SPG Canada

Among this year’s honourees, SPG Canada stood out for its medal performance and for how it has redefined its business to meet broker needs.

Its 5-Star MGA 2025 recognition reflects the themes that have defined this year’s survey, which include:

-

speed of service

-

governance strength

-

ability to fill coverage gaps in a shifting market

The multi-award-winning company has built its name on underwriting expertise, responsive service, and specialist product depth across sectors and regions. It is now the largest delegated underwriting authority enterprise in Canada, transacting more than $1 billion in premiums annually.

Under the leadership of president and CEO Cameron Copeland, SPG Canada has realigned its national operations by integrating five legacy MGAs (Cansure, Beacon, i3 Underwriting, Totten Insurance Group, and Anderson McTague & Associates) and restructuring around verticals and horizontals to reflect how brokers do business in 2025. The new structure is already supporting a steady rollout of product innovation, addressing the appetite gaps that brokers consistently flag as their biggest challenge.

In recent months, SPG Canada has:

- released new products in the SPGC Portal, including:

- small strata coverage (up to six units)

- rentals with an owner-occupant

- an earthquake deductible buy-down

- a soon-to-launch earthquake deductible assessment product

- a parametric earthquake solution for commercial properties, still rare in Canada’s market

- small strata coverage (up to six units)

- strengthened and expanded underwriting expertise and solutions in:

- mining

- commercial farms

- oil and gas contracting

- mining

- developed new niche programs for:

- waste management, including fleet auto coverage

- crane contractors, including fleet auto coverage

- waste management, including fleet auto coverage

This expansion is matched by a focus on speed in the SME segment. Through the newly launched SPG One team, brokers can now access rates, quote, bind, and issue decisions faster while still receiving personal guidance.

“Within a two-hour turnaround time, our underwriters will look at the submission, talk to the broker about why it works, why it doesn’t work, and what additional information we need,” Copeland explains. “We’re meeting the speed expectation but adding an educational element so they can grow into that middle-market space.”

Cameron CopelandSPG Canada

Technology is being integrated behind the scenes to improve submission flow and workload allocation. The company is moving to a single platform built to leverage AI to triage incoming files, while underwriting decisions remain with people. “We’re not saying technology first; we’re saying people first,” Copeland adds. “We’ve always been a relationship business, and I think that’s not going anywhere.”

On the compliance side, Copeland said the company is well-positioned as regulatory scrutiny on MGAs increases. “We are licensed corporately and individually as may be required in each jurisdiction across the country. We have full separation of duties across underwriting and claims operations and finance functions, and we run at near-public company standards of governance and compliance.”

For SPG Canada, the measure of quality is SOC compliance (System and Organization Controls, an independent audit standard that assesses data security and governance), which goes beyond individual carrier audits.

That people-first focus carries into internal development. SPG Canada runs training programs for its underwriting teams that emphasize both technical and soft skills. “If you can’t get the communication right from the person you’re dealing with, you’re not going to come back. But if someone says, ‘Let me look into this and find a solution,’ that’s what builds trust.”

When asked what keeps brokers coming back, Copeland’s response is direct: “Great people with a can-do attitude who have the expertise and knowledge to offer solutions,” he says. “This also includes bringing the strongest and broadest product and capacity to the table.”

Conclusion: where the real differentiation lies

In recent months, SPG Canada has:

-

Stability signals maturity: Flat usage doesn’t mean stagnation; it confirms MGAs are now an entrenched layer of distribution that brokers rely on for specific value.

-

Differentiation will come through service delivery: With products and appetite converging, speed of response, claims execution, and transparency are where competition will play out.

-

Governance is a market driver: As FSRA and other regulators sharpen oversight, carriers and brokers are already factoring compliance strength into partner selection.

-

Capacity is shifting, not unlimited: Carriers are expanding delegated authority, but are selective; MGAs must prove underwriting discipline to secure and keep that backing.

-

Broker trust hinges on human service: Brokers consistently engage MGAs for niche risks and responsiveness, confirming that relationships and judgment still carry weight alongside portals.

-

Profitability drives rewards: In addition to volume, carriers are increasingly using Contingent Profit Commissions to recognize MGAs that consistently deliver profitable books of business.

The Top MGAs in Canada | 5-Star Brokers on MGAs

5-Star MGAs

Ability to place niche or emerging risks

- Agile

- Aurora Underwriting Solutions

- Burns & Wilcox

- CFC

- Chutter Underwriting Services

- Forward Insurance

- Maxx Group MGA

- Special Risks Insurance Managers

- Trinity Underwriting

Compensation (commission, bonuses, profit-share, etc.)

- Aurora Underwriting Solutions

- CFC

- Maxx Group MGA

- Trinity Underwriting

Geographical reach

- Agile

- Aurora Underwriting Solutions

- Burns & Wilcox

- Chutter Underwriting Services

- Forward Insurance

- Maxx Group MGA

- Trinity Underwriting

Marketing support

- Aurora Underwriting Solutions

- Burns & Wilcox

- CFC

- Maxx Group MGA

- Trinity Underwriting

Overall responsiveness

- Aurora Underwriting Solutions

- Burns & Wilcox

- CFC

- Chutter Underwriting Services

- Forward Insurance

- Maxx Group MGA

- PAL

- Trinity Underwriting

Pricing

- Aurora Underwriting Solutions

- Burns & Wilcox

- CFC

- Chutter Underwriting Services

- Forward Insurance

- Maxx Group MGA

- PAL

- Special Risks Insurance Managers

- Trinity Underwriting

Range of products

- Agile

- Aurora Underwriting Solutions

- Burns & Wilcox

- CFC

- Chutter Underwriting Services

- Forward Insurance

- Maxx Group MGA

- PAL

- Trinity Underwriting

Reputation

- Agile

- Aurora Underwriting Solutions

- Burns & Wilcox

- CFC

- Chutter Underwriting Services

- Forward Insurance

- Maxx Group MGA

- PAL

- Trinity Underwriting

Technical expertise and product knowledge

- Agile

- Aurora Underwriting Solutions

- Burns & Wilcox

- CFC

- Chutter Underwriting Services

- Forward Insurance

- Maxx Group MGA

- PAL

- Trinity Underwriting

Technology/automation

- Aurora Underwriting Solutions

- Forward Insurance

- Maxx Group MGA

- Trinity Underwriting

Specialization

Accident and health

- Maxx Group MGA

Gold - CFC

Silver - Special Risks Insurance Managers

Bronze

Cannabis

- Burns & Wilcox

Gold

Commercial auto/transportation/trucking

- Special Risks Insurance Managers

Gold - Agile

Silver - Aurora Underwriting Solutions

Bronze

Construction

- Forward Insurance

Gold

Contractors

- Forward Insurance

Gold

- Chutter Underwriting Services

Bronze

Cyber

- CFC

Gold - Forward Insurance

Silver

Directors and officers

- Forward Insurance

Gold

- CFC

Bronze

Energy

- Burns & Wilcox

Gold

- Forward Insurance

Bronze

Environmental

- Forward Insurance

Gold

General liability

- Special Risks Insurance Managers

Gold - Forward Insurance

Silver

High net worth

- Agile

Silver

Hospitality

- PAL

Silver - Agile

Bronze

Management liability

- Trinity Underwriting

Gold

- CFC

Bronze

Marine

- Forward Insurance

Silver

Non-profit

- CFC

Bronze

Professional liability

- CFC

Gold - Forward Insurance

Silver - Special Risks Insurance Managers

Bronze

Program business

- Trinity Underwriting

Gold - Agile

Silver

Property (commercial)

- Forward Insurance

Gold

- Agile

Bronze

Real estate

- Aurora Underwriting Solutions

Silver - Forward Insurance

Bronze

Small business

- Forward Insurance

Gold - Special Risks Insurance Managers

Silver - Trinity Underwriting

Bronze

All Stars

- Aurora Underwriting Solutions

- Maxx Group MGA

Brokers’ Pick

- Forward Insurance

Course of construction

Insights

-

Steve Masnyk

Steve Masnyk

Executive Director

Canadian Association of Managing General Agents (CAMGA)

Methodology

Insurance Business Canada conducted a survey of brokers nationwide to determine the best businesses in the wholesale distribution channel. The survey asked respondents to rate the performance and service of each of their wholesale partners on a scale of 1 (poor) to 5 (excellent) against the following 10 criteria:

-

ability to place niche or emerging risks

-

compensation (commissions, bonus, profit share, etc.)

-

geographical reach

-

marketing support

-

overall responsiveness

-

pricing

-

range of products

-

reputation

-

technical expertise and product knowledge

-

technology or automation

The MGAs that earned an average score of 4.0 or greater in at least one category were awarded a 5-Star designation. MGAs that received an average score of 4.0 or greater in all categories received an All-Star designation. Brokers were also asked to rank their top three MGAs across 20 major types of insurance. Brokers also named the top insurance products offered by an MGA. Based on brokers’ feedback, IBC calculated the top three winners for each type of insurance and awarded gold, silver, and bronze medals to those wholesale brokers and MGAs. The three insurance products that received the most votes from brokers were awarded the Brokers’ Pick medal.

Keep up with the latest news and events

Join our mailing list, it’s free!