The Best Insurance Brokers in Canada

Jump to winners | Jump to methodology

Setting the pace

Insurance clients are setting new terms of service in 2025. Expertise and personal advice outweigh price and brand, even as digital options multiply.

The broker relationship remains essential; however, Insurance Business Canada’s 2023–25 data shows that trust comes with rising expectations about how service is delivered.

Key takeaways for brokers

-

Own the placement: clients expect brokers to lead insurer selection

-

Service defines the best: coverage, expertise, and personalized advice set the benchmark

-

Sell reassurance: more clients are willing to pay for peace of mind

-

Reframe cost discussions: position price within the value of protection and guidance

-

Stay ahead of risk: proactive recommendations distinguish trusted advisors

-

Stand by clients in claims: advocacy during difficult moments cements relationships

Reflecting on what it takes to stand out in Canada’s broker market, Mainstay Insurance Brokerage owner, Dave Patriarche, says, “What makes the best the best is they are very specialized in whatever it is they do. It’s not about selling lots of policies or making a ton of money but knowing their field as well as anyone.”

How Canada’s best insurance brokers shape the client experience

Canada’s insurance distribution sector was valued at just over $11 billion in 2025, according to IBISWorld. That reflects compound annual growth of 2.3 percent from 2019 to 2024. Distribution accounts for a meaningful slice of Canada’s finance and insurance sector, which makes up more than 7 percent of national GDP, according to Statistics Canada.

The numbers suggest stability, yet the reality for distributors has been one of constant adjustment.

Brokers and carriers are adapting to:

-

record climate losses

-

tighter regulatory frameworks such as the Office of the Superintendent of Financial Institutions’ (OSFI) new capital rules and IFRS 17

-

inflation

-

digital transformation

The industry has turned to consolidation, technology investment, and expanded risk advisory services to stay ahead. Distribution is evolving, and the best insurance brokers are channelling those currents into opportunities for their clients.

IBC tapped into its thousands-strong readership base to identify the brokers nationwide who have earned client trust. Readers nominated their brokers and rated them across six key service criteria. Those with an average score of 4 or higher earned a place on the third annual Top Insurance Brokers’ list.

Six ways IBC’s best insurance brokers earn client trust

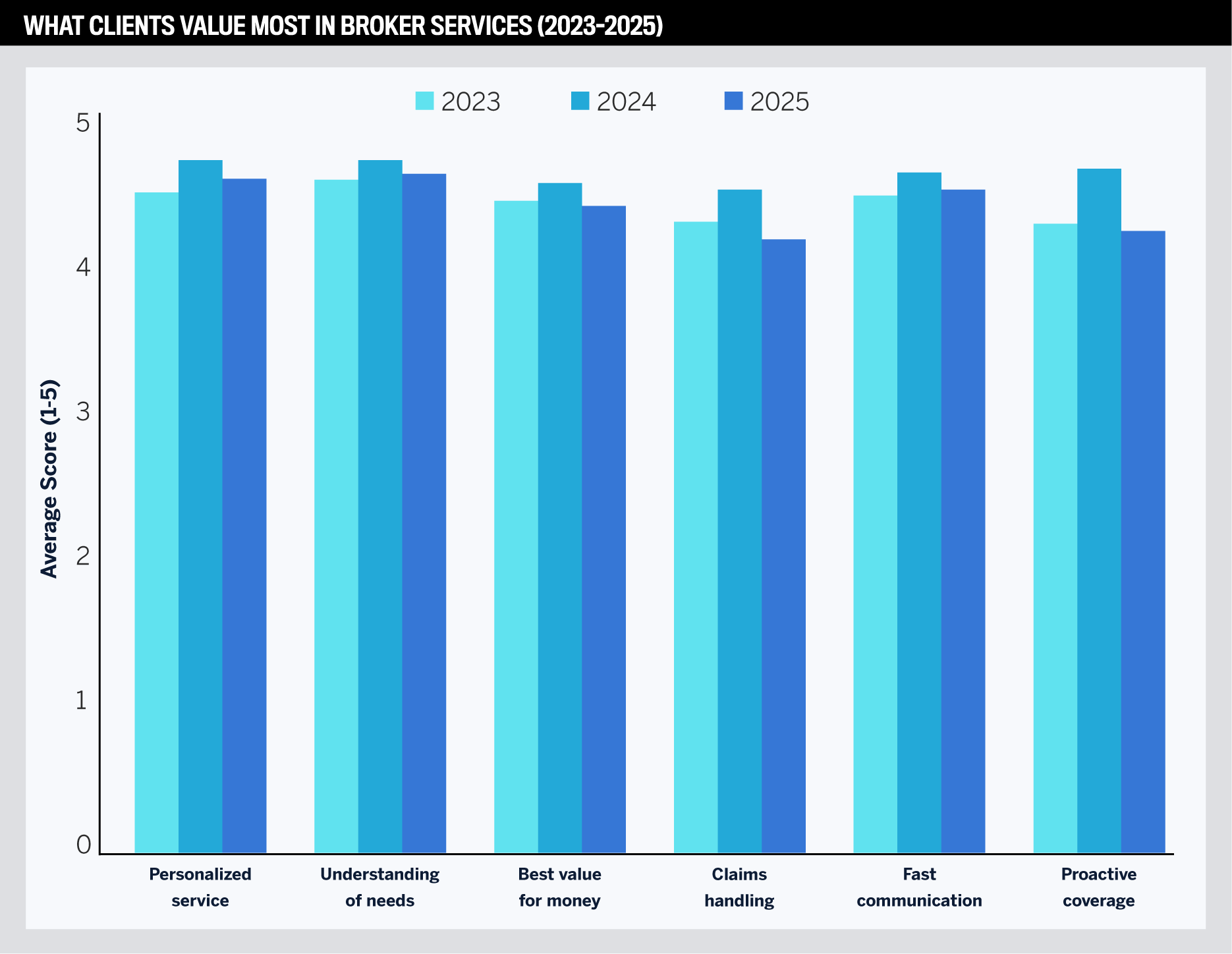

Clients in 2025 say the best brokers are the ones who understand their coverage needs and share advice that feels personal. Communication, value, and proactive guidance follow close behind, with claims support still viewed as an essential part of the package. Respondent brokers rated using a scale where 1 is not important and 5 is most important.

- Understanding coverage needs

- Data: Highest score in 2025 at 4.90; also led in 2023 (4.87) and tied for first in 2024

- What it means: Clients place the greatest value on brokers who truly understand their coverage requirements. Leading brokers demonstrate this by tailoring policies to specific risks and ensuring clients feel assured that their needs are met.

- Data: Highest score in 2025 at 4.90; also led in 2023 (4.87) and tied for first in 2024

- Personalized service

- Data: 4.86 in 2025; top-ranked in 2024 at a perfect 5.00

- What it means: Personalization is central to client trust. The best brokers distinguish themselves by offering individual attention and bespoke service.

- Data: 4.86 in 2025; top-ranked in 2024 at a perfect 5.00

- Fast and easy communication

- Data: 4.78 in 2025; peaked at 4.90 in 2024

- What it means: Clients expect quick, clear communication as part of professional service, and brokers who excel here reinforce reliability and accessibility.

- Data: 4.78 in 2025; peaked at 4.90 in 2024

- Value for money

- Data: 4.66 in 2025, compared with 4.84 in 2024 and 4.71 in 2023

- What it means: Clients care about cost, but value is about more than just price. Top brokers deliver value by balancing competitive premiums with strong coverage and service, showing clients that protection is as important as affordability.

- Data: 4.66 in 2025, compared with 4.84 in 2024 and 4.71 in 2023

- Proactive advice

- Data: 4.49 in 2025, down from 4.92 in 2024

- What it means: Clients want brokers who anticipate coverage gaps and recommend solutions before problems arise. Those recognized on the 2025 list excel at foresight, helping clients adapt to emerging risks and new exposures.

- Data: 4.49 in 2025, down from 4.92 in 2024

- Claims support

- Data: 4.42 in 2025; peaked at 4.78 in 2024

- What it means: While ranked lowest, clients expect brokers to stand with them through difficult moments, and the best brokers demonstrate this by being effective advocates when a claim occurs.

- Data: 4.42 in 2025; peaked at 4.78 in 2024

For industry leader Patriarche, IBC’s survey findings highlight a long-standing divide between transactional brokers and those who act as true advisors.

“The majority of our industry are order takers,” he says. “The clients say, ‘I have this; give me more of that,’ and the advisor just does exactly what they’re told. But most of the time that isn’t what the client really needs.”

He argues that top brokers set themselves apart by questioning assumptions and steering clients toward better outcomes. “The leading people tend to ask questions and listen and basically help them find the right solution, not the easy solution. And there’s a massive difference between the two.”

Patriarche also sees specialization as a marker of value. He says, “Being a specialist helps you understand the situation, the markets, and everything else better. If you’ve got that down, you don’t have to work very hard; you’re not struggling to find new clients.”

This year’s Top Insurance Brokers echoed that view, stressing the qualities clients ranked highest:

-

listening carefully

-

asking better questions

-

treating each case as distinct

For British Columbia-based Top Insurance Broker 2025 Jamil Karimani, managing vice president at BFL Canada, the starting point is always the client. Survey respondents credited his reputation for trust, attentiveness, and proactive advocacy, placing him and his team among the benchmarks for client service in Vancouver’s market.

He makes a point of asking open-ended questions about the company’s background, the experience of its management team, their key performance indicators, and their philosophy toward risk.

These conversations also explore how much risk a client is comfortable retaining versus transferring to the market, along with their past experiences with brokers, insurers, and claims.

By grounding the discussion in those details, he can tie advice to a client’s risk tolerance and the realities of an evolving market. “It’s all about equipping their management team with decision-making capabilities that fulfill their contractual indemnity requirements but also establishing that trust and reliability in what they feel is necessary from their broker advocacy partner,” he explains.

Jamil KarimaniBFL CANADA Risk and Insurance Services

Fellow Top Insurance Broker 2025 Tara Khodaparast, an account executive at Concord, Ontario-based Connect Insurance, treats every new interaction as a discovery conversation.

Survey respondents emphasized her ability to make complex insurance decisions accessible, building loyalty through trust, reassurance, and personal connection. She asks open-ended questions to understand a client’s lifestyle, concerns, and past experiences with insurance, paying close attention to what has frustrated them and what has provided assurance.

That approach allows her to shape recommendations around individual needs while making sure clients feel genuinely heard. “I don’t think insurance should be just black and white. I like to see insurance as something so colourful and fun, and it gives you peace of mind,” she says.

For her, tailoring advice means matching solutions with a client’s real priorities.

Tara KhodaparastConnect Insurance

Brokers in the driver’s seat

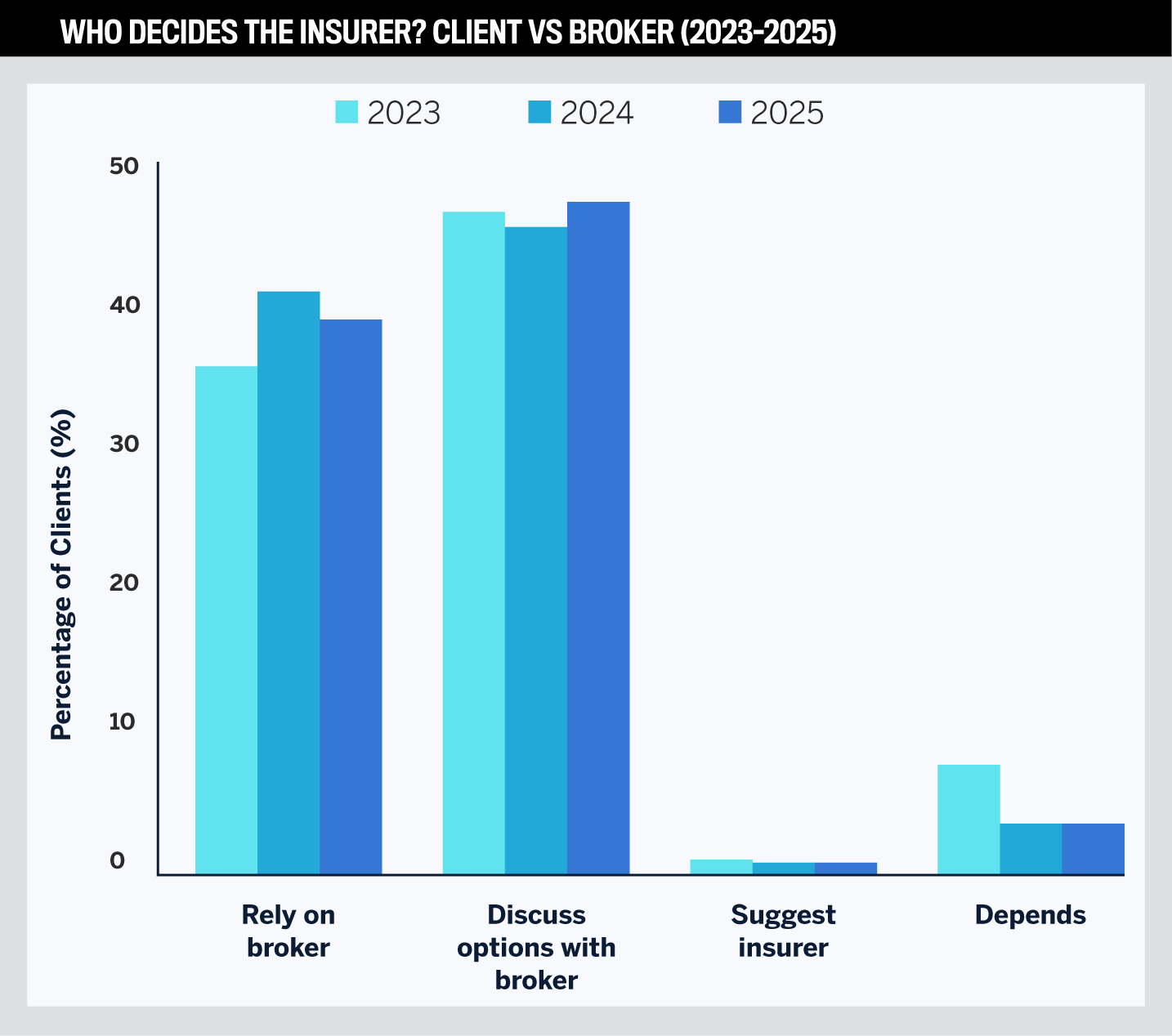

Clients overwhelmingly trust their brokers to guide insurer selection. The majority either rely entirely on their broker’s judgment or make the decision together after reviewing options, underscoring the broker’s role as both advisor and advocate in navigating the market.

- Broker as trusted decision-maker

- Data: 43 percent of clients in 2025 said they always rely on their broker to decide which insurer to use (up from 39 percent in 2023).

- What it means: Confidence in broker expertise is rising. Clients see brokers as experts who can weigh underwriting appetite, financial strength, and service standards better than they can on their own. Award-winning brokers have earned that trust through consistent guidance.

- Data: 43 percent of clients in 2025 said they always rely on their broker to decide which insurer to use (up from 39 percent in 2023).

- Collaborative decision-making

- Data: 52 percent of clients in 2025 said they discuss options with their broker and decide together (steady across all three years).

- What it means: Collaboration is the dominant model. Clients want to be involved but rely on brokers to frame the options and explain the trade-offs. Top brokers excel at this consultative role, combining technical knowledge with the ability to translate coverage choices into clear, client-centred recommendations.

- Data: 52 percent of clients in 2025 said they discuss options with their broker and decide together (steady across all three years).

- Minimal direct influence by clients

- Data: Only 1 percent of clients across three years said they suggested which insurer to use themselves.

- What it means: Very few clients feel equipped to choose insurers without broker input. This highlights the broker’s central role in simplifying a complex marketplace and providing assurance that clients are getting the best fit.

- Data: Only 1 percent of clients across three years said they suggested which insurer to use themselves.

- Case-by-case scenarios

- Data: 4 percent in both 2024 and 2025 (down from 8 percent in 2023) said it depends on circumstances.

- What it means: Fewer clients are taking a conditional approach, indicating greater consistency in leaning on broker expertise. When circumstances do play a role, such as prior claims or personal preferences, brokers remain the anchor in final decision-making.

- Data: 4 percent in both 2024 and 2025 (down from 8 percent in 2023) said it depends on circumstances.

Clients’ reliance on brokers to choose insurers is also tied to the structure of the Canadian market and the technology behind it. As Patriarche explains, “In Canada, we’re licensed by province, so I can only sell insurance in Ontario. They can have employees in other provinces, but I can only sell here. Same with the United States, same with the UK and Europe.”

That framework makes the broker’s role in placement especially critical. He also argues that the industry’s technology gap reinforces dependence on brokers. “Basically, they are running on old legacy mainframe COBOL systems, so 1970s technology, and that’s a huge problem. There’s very little innovation in product or service or offering here, so compared to the US, their technology is much more advanced.”

Patriarche’s view highlights a tension that also runs through IBC’s survey results. Clients trust brokers to weigh the market and guide insurer selection, yet they also want confidence that the decision reflects their own priorities.

The best brokers manage that balance of authority and collaboration. For BFL’s Karimani, trust is at the heart of the client relationship. Clients lean on their broker’s expertise, but they also want to feel involved in the outcome.

He sees his role as an extension of the client’s risk management team, providing education throughout the year, presenting deductible and expenditure options, and equipping management with insights on emerging trends in both domestic and international markets.

He adds that technical expertise on its own does not create trust. “Trust is really achieved in several ways. High character and high competency, but it’s also exuding our company’s core values, which are respect for diversity of thought, integrity, community service, collaboration, excellence, and entrepreneurial spirit.”

Aligning those values with a client’s own principles, he says, lays the groundwork for lasting partnerships.

Connect Insurance’s Khodaparast also sees her role as both advisor and educator. While clients often rely on her judgment, she believes they should also feel informed and confident in the choices they make.

To achieve that, she breaks down complex insurance terms into plain language and explains the reasoning behind her recommendations. She says this approach builds long-term relationships because clients know she is working with them, not just for them.

“I also view my clients as friends in a way, because the way I talk to them, I feel like I make them more comfortable. And they just naturally open up to me after that, too.”

Coverage first, cost second

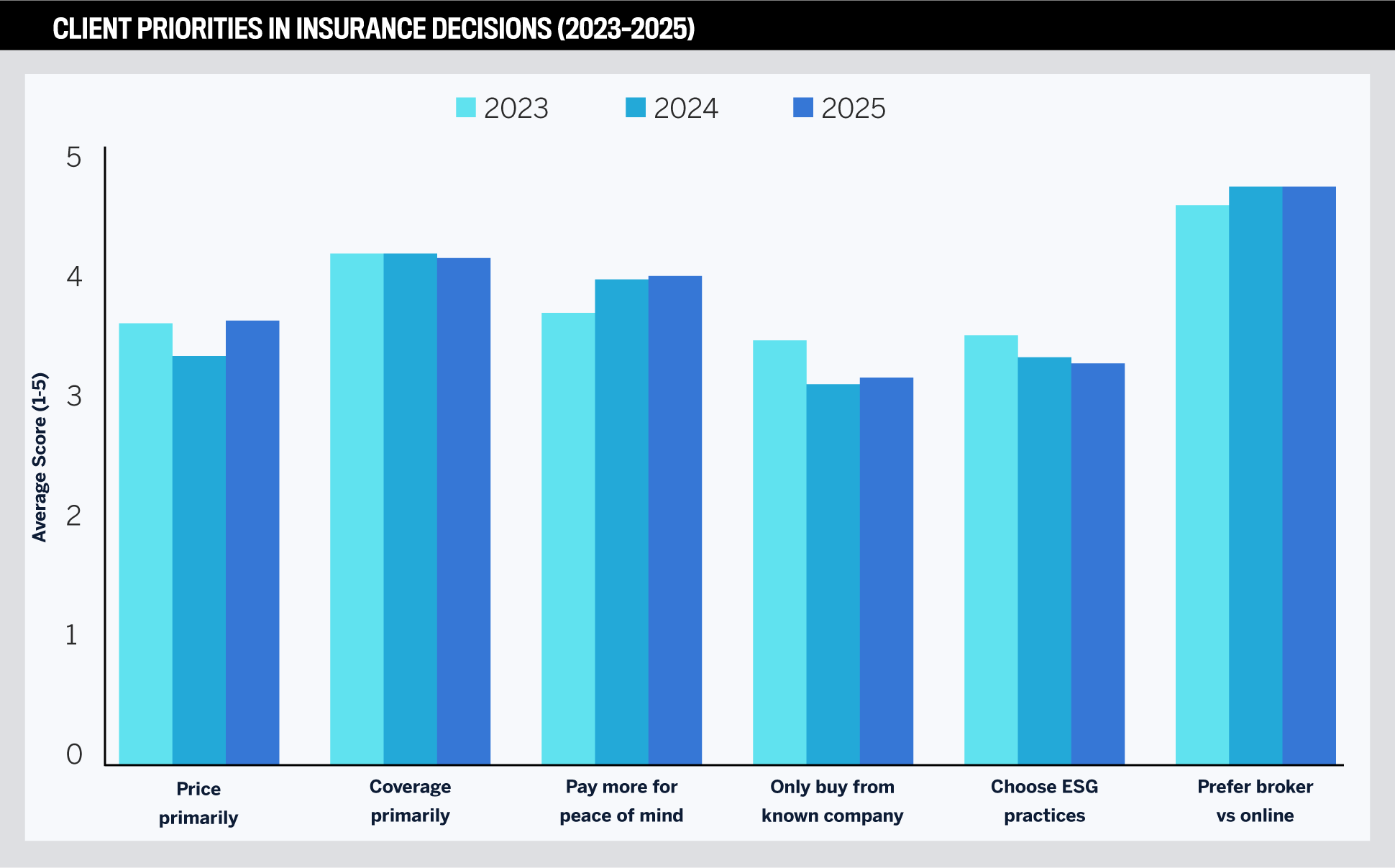

- Preference for broker interaction

- Data: 4.84 in 2025; 4.85 in 2024; 4.70 in 2023

- What it means: Across three years of data, the strongest signal is that clients want a broker they can talk to, not an online platform. For award-winning brokers, this reinforces the enduring importance of human connection and personal service, even in an increasingly digital market.

- Data: 4.84 in 2025; 4.85 in 2024; 4.70 in 2023

- Coverage over price

- Data: Coverage scored 4.25 in 2025 (highest among decision factors), while price scored 3.73. Both measures have been stable across three years.

- What it means: Clients prioritize the protection insurance provides above the cost alone. Top brokers succeed by educating clients on the value of comprehensive coverage and steering decisions toward fit, not just affordability.

- Data: Coverage scored 4.25 in 2025 (highest among decision factors), while price scored 3.73. Both measures have been stable across three years.

- Peace of mind matters

- Data: Willingness to pay more for peace of mind scored 4.09 in 2025, up from 3.80 in 2023.

- What it means: Clients are prepared to invest in policies that provide confidence and security. Award-winning brokers tap into this mindset by positioning insurance as long-term protection rather than a short-term expense.

- Data: Willingness to pay more for peace of mind scored 4.09 in 2025, up from 3.80 in 2023.

- Brand recognition plays a limited role

- Data: “Only buy from a company I’ve heard of” scored 3.26 in 2025, down from 3.56 in 2023.

- What it means: While reputation still matters, clients rely more on broker judgment than brand familiarity. The trust they place in brokers is stronger than the name recognition of insurers, highlighting the broker’s influence in shaping client choices.

- Data: “Only buy from a company I’ve heard of” scored 3.26 in 2025, down from 3.56 in 2023.

- Social and environmental practices

- Data: 3.38 in 2025, down from 3.61 in 2023.

- What it means: ESG considerations are present but secondary to core concerns such as coverage and service. Brokers who can connect insurer sustainability initiatives to client values have an opportunity to differentiate, but it is not yet a decisive factor for most clients.

- Data: 3.38 in 2025, down from 3.61 in 2023.

- Price sensitivity exists, but not primary

- Data: 3.73 in 2025; steady compared with 3.72 in 2023.

- What it means: Clients weigh price, but not above coverage or broker advice. While cost matters, brokers’ conversations should always pivot to protection, value, and service.

- Data: 3.73 in 2025; steady compared with 3.72 in 2023.

Patriarche sees IBC’s survey findings borne out in practice in his capacity as founder of the Canadian Group Insurance Brokers Association, which trains brokers nationwide. He notes that many brokers still rely on outdated tools, which makes personal relationships with clients even more important.

“When I ask simple questions, such as ‘Do you know what a CRM is?’, less than 10 percent said yes. So, 90 percent of people in our industry are just faking it. You don’t have to have a CRM, but it definitely makes you efficient, and that’s 30- or 40-year-old technology.”

Patriarche also believes AI and automation will shape the future, but only gradually. “With AI and automation, we’ll get there, but it’s going to be slow,” he says. “And the big challenge is that so much of the backend, especially in insurance, is still running on legacy mainframe systems.”

The intersection between digital progress and human connection is where this year’s winners offered perspective. Their views show how brokers are adapting to new tools while keeping personal service at the forefront of client relationships.

Karimani argues that technology can assist brokers but cannot replace trust and authenticity. Digital platforms may streamline tasks, yet he stresses the core value of a broker lies in empathy, partnership, and insight. To him, the job is about listening closely, explaining coverage in plain terms, and keeping pace with a client’s changing goals.

He adds that brokers maintain that bond through regular check-ins and by tailoring advice to emerging risks.

For Karimani, digital tools and human advocacy work best together. Technology handles efficiency, while brokers provide the context and nuance that only a trusted advisor can offer. Khodaparast also acknowledges that technology is reshaping insurance, but she frames it as a support tool rather than a replacement. For her, digital platforms and AI can make processes faster and more efficient, yet the essence of the broker’s role remains unchanged. “No algorithm can replace genuine human empathy,” she says.

She believes the future lies in blending innovation with a personal touch, where technology enhances service but never substitutes for authentic advice and being invested in clients’ well-being.

Best insurance brokers guide clients through a market in transition

Canada’s insurance industry entered 2025 with scale and resilience, but it also faces one of its most demanding environments in recent memory.

Catastrophic weather losses, affordability concerns in auto insurance, and talent shortages are shaping operations, while digital innovation and new capital are opening opportunities.

Property and casualty (P&C) insurers are adjusting to record catastrophe payouts, commercial lines are easing after years of hard-market pricing, and life and health insurers are expanding coverage through product innovation.

For the best insurance brokers, guiding clients through this volatility while maintaining trusted relationships has become a defining measure of success.

Broad industry trends

-

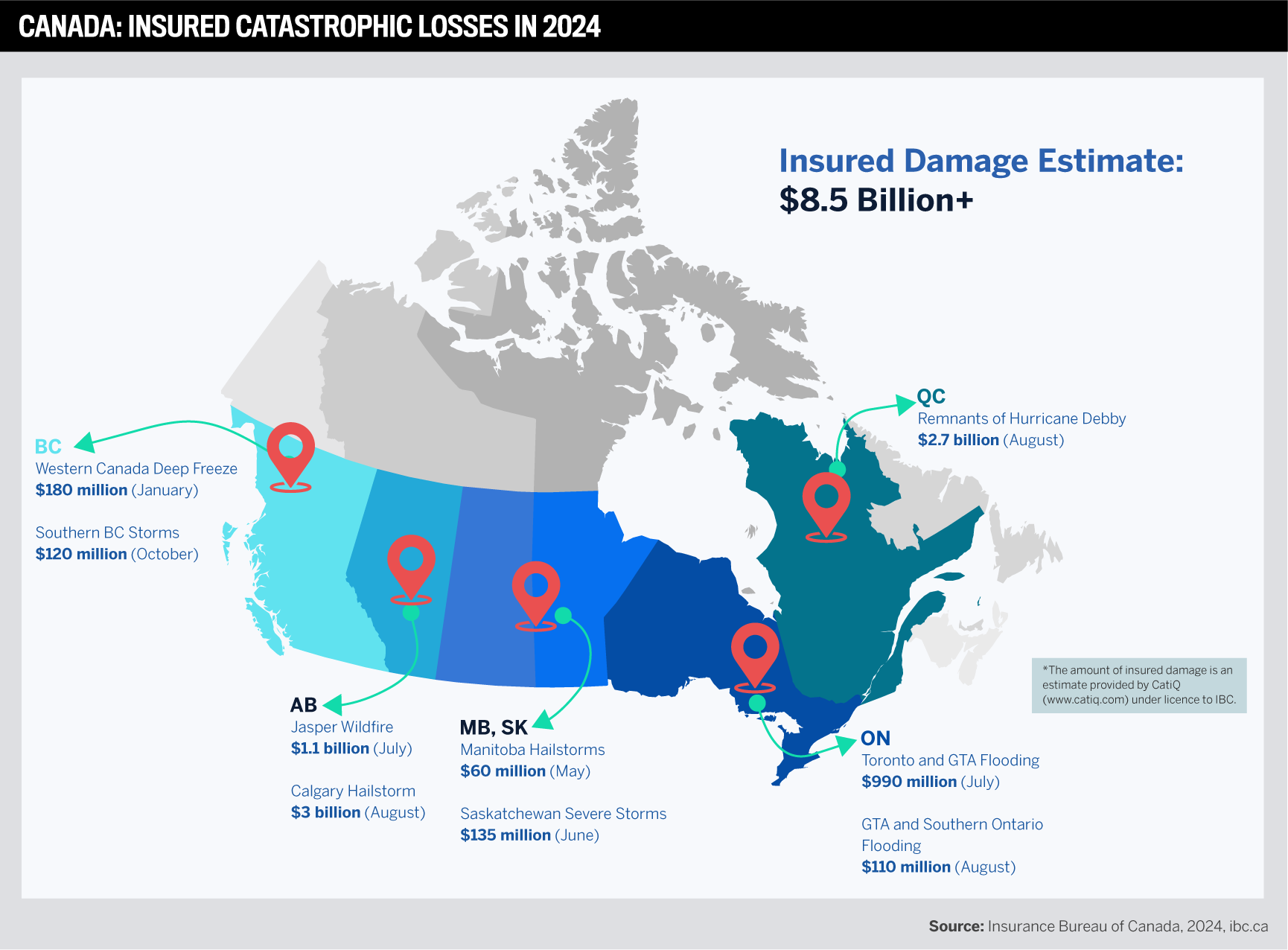

Record catastrophe payouts: 2024 set a record with over $8 billion in insured damage from severe weather events; climate change has made catastrophe risk a leadership issue, requiring direct oversight from the top of the organization.

-

Market cycle turning: After years of rate hikes, competition is intensifying in 2025, with some commercial lines seeing premium declines.

-

Digital adoption: Insurers are deploying AI, telematics, and digital platforms to improve underwriting, claims, and distribution.

-

Talent shortage: Brokers and carriers alike are struggling to fill skilled roles, particularly in commercial lines.

-

Regulatory tension: Provinces are tightening oversight on auto rates, and Ottawa is advancing a pharmacare plan that could reshape private drug coverage.

P&C insurance

P&C remains the backbone of Canada’s insurance sector, with nearly 200 private insurers writing billions in annual premiums. Climate volatility and inflation in claims costs dominate 2025.

-

Climate-driven claims: Calgary’s 2024 hailstorm caused about $2.8 billion in insured damage, part of the record-breaking year; wildfire and flood exposures continue to test capacity.

-

Home insurance: Premiums rose roughly 5 percent year-on-year in Q1 2025, driven by higher rebuild costs; some flood-prone properties face limited availability.

-

Profitability pressure: Combined ratios are hovering near 100 percent, leaving underwriting results close to break-even.

-

Distribution: Direct-to-consumer channels are growing, but brokers remain dominant, especially in complex risks.

-

Innovation: Usage-based auto insurance and climate-resilient property coverages are expanding as insurers adapt to consumer demand.

Commercial insurance

After a prolonged hard market, 2025 brought the first signs of relief for Canadian businesses purchasing coverage.

-

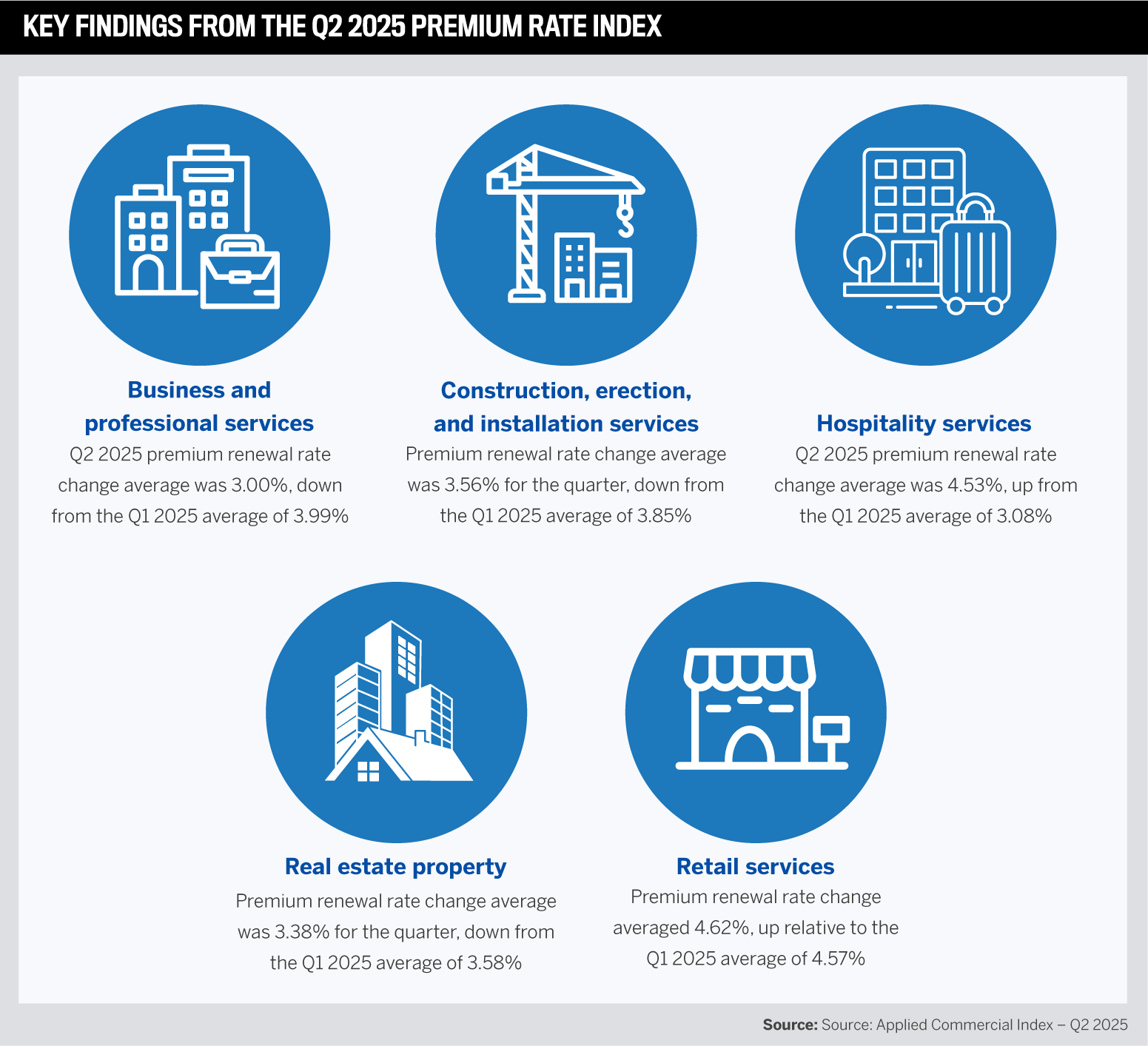

Premium moderation: Q2 2025 saw average commercial rates fall 4 percent, with property down 6 percent and casualty down 2 percent.

-

Capacity influx: New entrants, MGAs, and capital from global carriers are fueling competition.

-

Coverage shifts: Broader terms and higher sub-limits are returning in competitive classes, while exclusions for PFAS and wildfire risks are spreading.

-

Persistent challenges: Heavy industry, high-hazard property, and trucking fleets still face tough underwriting and elevated premiums.

-

Cyber insurance: Premiums declined about 3 percent in mid-2025 as capacity expanded and insureds strengthened cybersecurity controls.

Life and health insurance

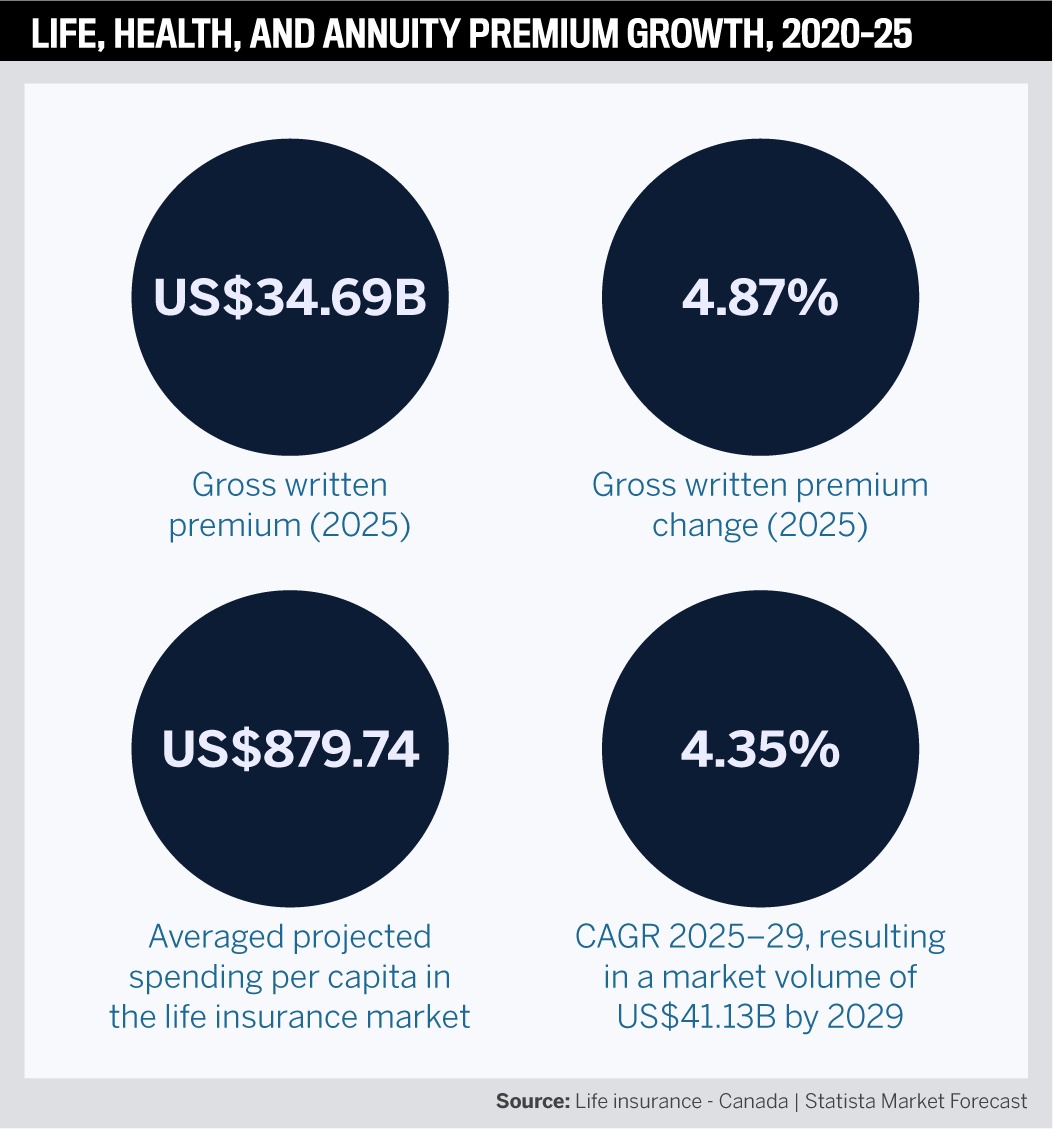

Life and health insurers are financially solid, with over $1 trillion in assets and steady growth in premiums. Demand for protection and wellness products remains high.

-

Premium growth: Industry premiums and annuity contributions rose to $157 billion in 2023, with health insurance up 8.7 percent and life up 6.4 percent.

-

Life insurance sales: Term policies now make up 75 percent of policies in force by count, while whole life accounts for two-thirds of premium revenue.

-

Coverage gaps: Surveys show 57 percent of Canadians feel underinsured, creating growth potential.

-

Health benefits: Employer plans face cost pressures from specialty drugs and mental health claims; individual health insurance is gaining traction.

-

Innovation: Digital-first underwriting, AI-based fraud detection in health claims, and wellness incentives are reshaping offerings.

Auto insurance

Auto remains the most politically sensitive insurance line in Canada, with affordability the central issue.

-

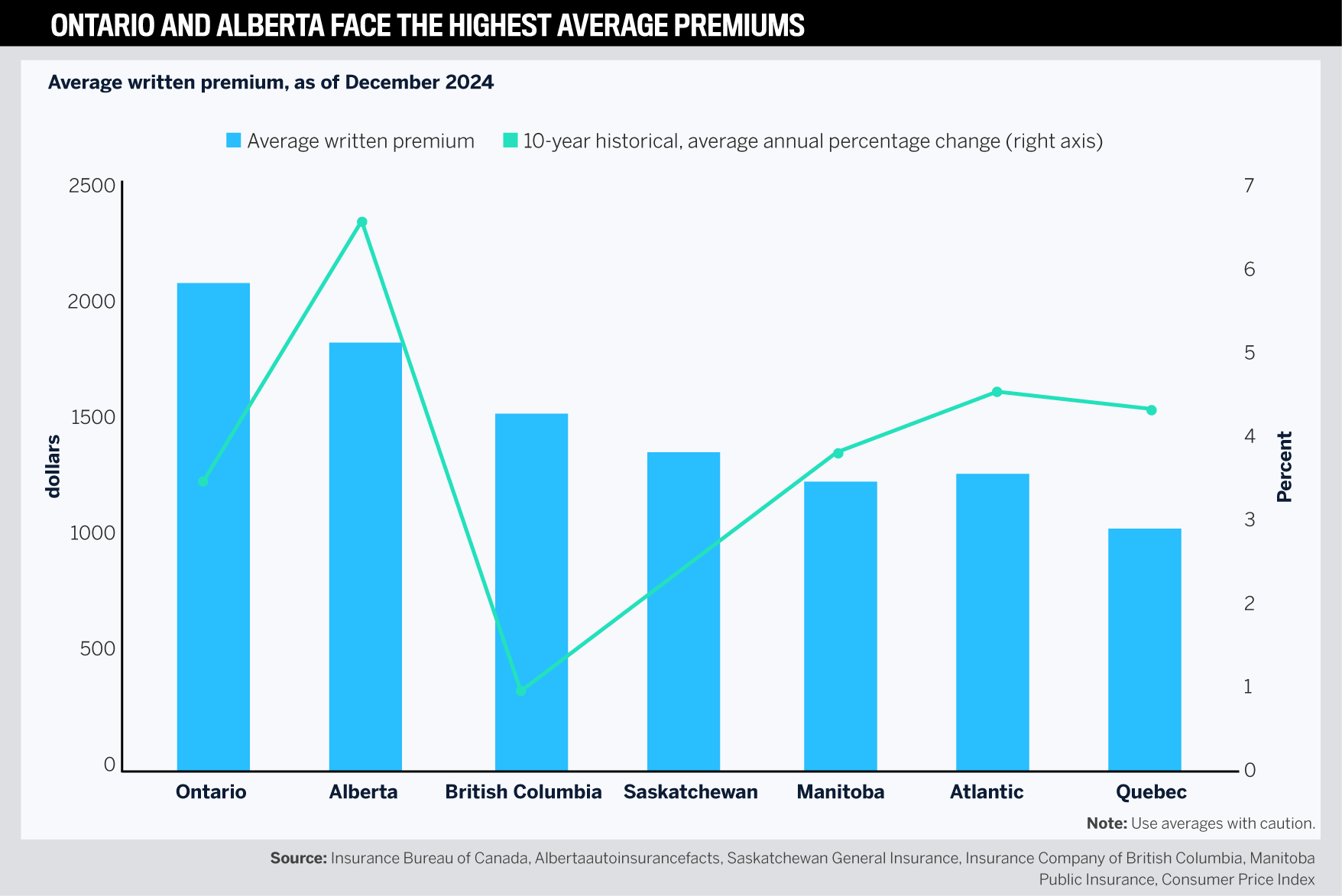

Premium hikes: Personal auto rates rose an average of 13 percent year on year in Q1 2025, with Ontario up nearly 15 percent.

-

Cost drivers: Repair costs for tech-heavy vehicles, a surge in theft, and normalized accident frequency are fueling loss inflation.

-

Regional disparities: Average annual premiums now top $2,000 in Ontario, compared with under $800 in Quebec.

-

Regulatory pushback: Alberta lifted its temporary rate freeze in 2024 and is weighing structural reform; Ontario is exploring product redesigns and fraud reduction.

-

Risk mitigation: Insurers are mandating or incentivizing anti-theft devices, and telematics programs are expanding.

Conclusion: how Canada’s broker channel has been successful

-

Tech helps, but trust still wins.

-

Specialization is the new edge.

-

Advisors beat order takers.

-

Client experience drives loyalty.

-

Brokers translate industry change into client strategy.

The Best Insurance Brokers in Canada

- Alexander Hutchison

Caldwell Insurance Services - Bobbee-Jo Wood

Atlas York Insurance - Crystal Parisien

Ing & McKee Insurance - Denis Landry

Wilson Insurance - Fardin Ahmed

Link Insurance Glenbrook - Jack Schmidt

Wilson M. Beck Insurance Services - Karim Chandani

Wilson M. Beck Insurance Services - Karim Zein

HUB International - Kathy Dang

Surex - Kayla Thompson

Atlas York Insurance - Leah Jurgens

Atlas York Insurance - Morgan Roberts

RH Insurance - Richard Wahl

Nation North Insurance - Rose Freeman

Willow Insurance - Sarah Irwin

Aon Reed Stenhouse - Scott Romans

Ing & McKee Insurance - Tina Brenner

Ing & McKee Insurance - Tom Meier

Johnston Meier Insurance Agencies Group

Insights

-

Dave Patriarche

Dave Patriarche

Owner

Mainstay Insurance Brokerage

Methodology

Insurance Business Canada conducted its third annual search for the Top Insurance Brokers to discover the best brokers who act in their clients’ interests. From a diverse cross-section of insurance professionals, the IBC team had the opportunity to spotlight remarkable examples of passion, dedication, and commitment.

From May 19 to June 13, the IBC team undertook a rigorous marketing and survey process, leveraging its connections to thousands of readers across the country. Readers were asked to nominate their brokers and rate them on six key criteria.

The most voted-for brokers that received an average score of 4 or higher were named Top Insurance Brokers, who were recognized based not on revenue but rather on the service provided to their clients.

Keep up with the latest news and events

Join our mailing list, it’s free!