The Top Insurance Claims Carriers in the UK |

5-Star Claims

Jump to winners | Jump to methodology

Claim to fame

Storm-driven losses, surging motor repair costs and record payouts in life, protection and pet policies have raised the stakes across UK claims.

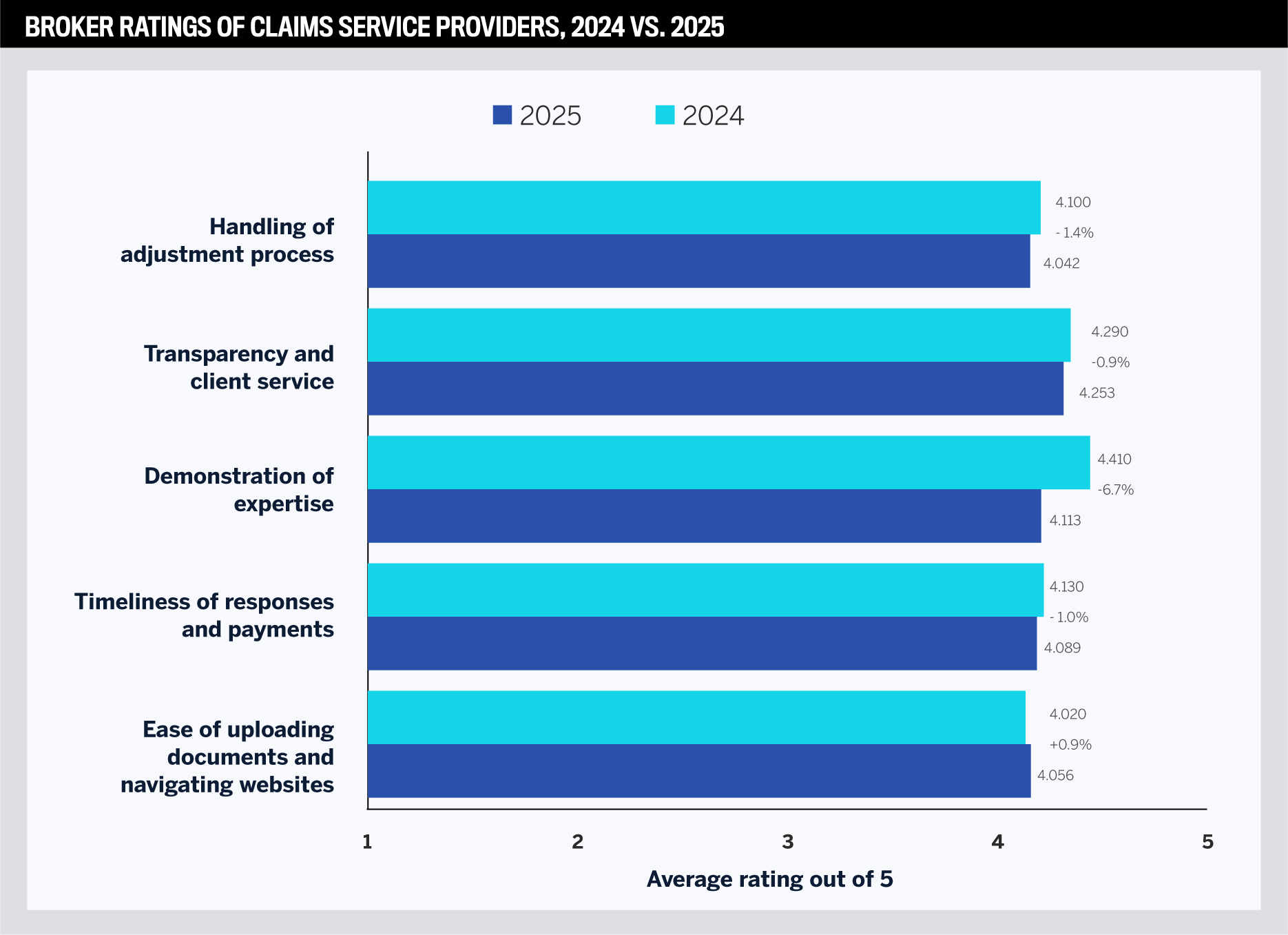

In Insurance Business UK’s 5-Star Claims 2025 survey, brokers rated most carriers as competent and reliable, yet they are watching for gains in speed, process and specialist knowledge. The top contenders earned 5-Star recognition by delivering on those broker priorities as volumes climbed and complexity increased.

This year’s report captures nationwide broker feedback on providers they worked with in the past 12 months. Brokers rated performance across five claims categories, and IB’s research team weighted those criteria based on what brokers value most. Providers with the highest overall scores were named 5-Star winners.

-

Transparency and client service leads in 2025: It holds the highest broker rating this year, while expertise led in 2024. Top carriers win confidence by keeping brokers informed with regular touchpoints and accessible contacts.

Talbot Jones managing director Richard Talbot-Jones reinforces why these factors topped broker priorities.

“Good, prompt communication is what we want most from a claims provider,” he says. “Ninety-five percent of the time, we, as brokers, are prompting insurers for updates. Across our agencies, we regularly ask for updates or send in notifications for claims and can wait weeks for a response.”

-

Demonstration of expertise eased back year over year: The carriers recognised as 5-Star are those where brokers still noted specialist judgement on complex claims.

On the subject of specialist expertise in a claims provider, Talbot-Jones says, “It’s important, but basic claims handling skill and ability would go a long way towards improving service. Often, specialist expertise is found in insurers that handle their own claims. These companies tend to perform much better on claims handling more generally because they keep the majority of it in-house.”

-

Speed and usability remain lower in the set: Ease of uploading documents and navigating websites ticked up slightly, while timeliness of responses and payments and handling of the adjustment process edged down. Leading claims carriers cut steps at intake, make document uploads work the first time and keep payment decisions moving.

For Talbot-Jones, fast turnaround is 24 hours. “I think different stages of claims handling should have different turnaround times. I don’t expect or need a 24-hour turnaround on everything, but at the early stages of a claim, I believe that speed is of the essence.”

-

Operational pain points persist: Ease of portals, payment speed and adjustment handling continue to trail relationship measures. Carriers that show verified gains on these fronts are well placed to lead next year’s results.

Following the pandemic, claims teams were heavily disrupted and attention shifted to business interruption claims, says Talbot-Jones.

“Since 2022, I’ve found claims service improving slightly, but it is still poor,” he adds. “We have lost clients because of poor claims service. More frustratingly, it often isn’t even the insurer’s fault. They’ve been let down by their nominated handler, but quite rightly, they have to take responsibility for choosing whom they outsourced claims handling to. Insurers, adjusters and TPAs need to really improve what they do.”

Industry overview

The UK insurance claims market is being reshaped by record weather events, increasing motor costs and growing demand in protection, pet and travel lines. Broker expectations for transparency, expertise and service are rising amid ongoing change. The latest data paints a picture of a sector dealing with higher volumes, higher payouts and more complex claim dynamics.

Weather-driven payouts hit records

Severe storms drove unprecedented home and property claims through 2024 and early 2025. Between January and April 2025, weather-related home insurance claims reached £226 million, the highest quarterly total on record and £67 million more than the previous record set in 2022.

-

Domestic property insurance payouts rose 20% year-on-year to £886 million, while business-related weather claims totalled £109 million, up £7 million from the prior year.

-

Across domestic and commercial property combined, insurers paid £1.5 billion in the first quarter, £170 million more than in the same period of 2024.

Storm Eowyn (January 2025), described by the Met Office as the most powerful windstorm in over a decade, was a major driver of these losses.

For the whole of 2024, weather-related claims reached £585 million, surpassing the previous record in 2022 by £77 million and £127 million higher than 2023. That year’s storm season brought 12 named storms, the most since 2015–16, prompting the ABI to call for long-term investment in flood defences.

Motor claims at all-time highs

Motor insurance remains under strain from high claims costs despite recent relief on premiums.

-

Insurers paid out a record £11.7 billion across 2.4 million claims in 2024, a 17% increase on the year before.

-

The average private motor claim rose 13% to £4,900, while the final quarter saw an all-time high of £5,300 per claim.

-

Vehicle repair costs reached £1.9 billion in Q4 and £7.7 billion for the full year, £1.5 billion more than in 2023.

-

Theft claims also climbed, with average payouts reaching £11,200 in Q4.

In parallel, the ABI’s premium tracker shows the average cost of motor insurance fell to £562 in Q2 2025, £60 less than a year earlier. Even with that decline, claims costs remain elevated due to more complex vehicle technology, inflation in parts and labour, and a shortage of skilled technicians.

The Financial Conduct Authority confirmed that higher claims costs, rather than profit-taking, were the main driver of past premium increases. Its review also identified poor practices in parts of the market, including low acceptance rates for storm damage claims and delays linked to outsourced services.

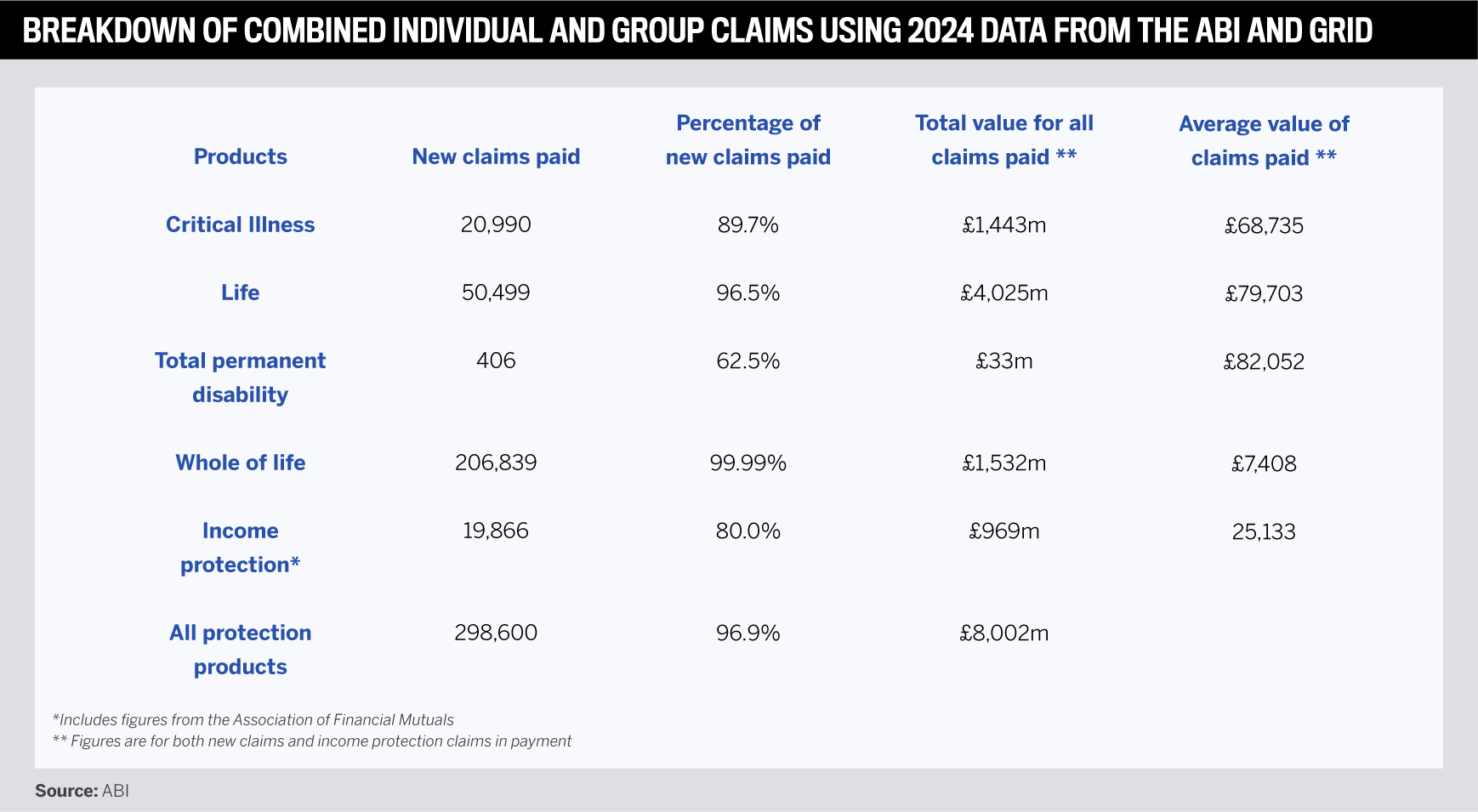

Protection payouts scaled up

Life and protection claims reached record levels in 2024, with insurers paying £8 billion across group and individual policies, the equivalent of £21.9 million per day. Individual payouts totalled £5.32 billion, a 10% increase on 2023, while the number of claims remained steady at 275,000. The average payout rose to £18,700.

-

Critical illness claims grew to £1.3 billion, with average payouts of £67,600.

-

Cancer remained the leading cause, making up 62% of cases and £812 million in payouts.

-

Income protection claims reached £204 million, up 16% year-on-year, with musculoskeletal issues the top cause at 34% and at least £32 million paid out.

-

The acceptance rate for individual claims held steady at 97.9%, in line with a decade of high payout ratios.

-

Common reasons for declined claims included non-disclosure of medical conditions or failing to meet policy definitions.

Pet and travel claims grew

Pet insurance continued its growth trajectory, with ABI members paying out £1.23 billion in 2024, a 4% increase from the year before and more than double the level of a decade ago. A record 1.8 million claims were notified, an average of 4,900 per day.

-

Dogs accounted for £933 million in payouts.

-

Cats, £232 million.

-

Other pets, £61 million.

The number of insured pet owners rose to 4.6 million, up 3% from 2023 and 33% higher than in 2019. Travel insurance claims also rose, with £472 million paid out across more than 500,000 cases in 2024. Medical expenses were the most common reason for claims, making up 34% compared to 29% a year earlier. The total value of medical claims reached £262 million, with an average payout of £1,528.

How the top insurance claims winners are leading the pack

Collaboration is the firm’s touchstone as it provides regular updates at key milestones and utilise their CRM team to schedule claim review meetings with both brokers and customers.

“True claims excellence comes from matching the right expertise to each unique situation,” says Judy O’Neill, chief claim officer for Travelers Europe. “Our claim professionals don’t just process cases – they partner with brokers and clients throughout the entire claim journey, leveraging years of specialised experience to navigate challenges and deliver optimal outcomes.”

Judy O’NeillTravelers Europe

Travelers is also focused on refining its processes, such as by innovation in motor claims, where it has implemented:

-

a roadside reporting app for motor vehicle incidents

-

one-stop reporting for simultaneous notification from the roadside to brokers/insurers/client fleet manager

-

discussions around liability, which can be agreed upon before the driver returns to their workplace

-

two-hour SLA for third-party capture, reducing credit hire claims

The firm has also made strides in accelerating responses, payments and the adjustment process. To achieve this, the subrogation team has been appointed as a secondary handler alongside their claim professionals when opportunities for recoveries arise, allowing them to start the recovery process as the first party element is being managed.

O’Neill explains, “This ensures the right touch occurs on a claim at the right time, and adopting a fast-track, light-touch philosophy to agreeing low-value claims, without lengthy investigations or documentation reducing the overall lifecycle of the claim, keeps costs down for the end customer and improves their net loss ratio.”

In addition, the expense control team has achieved significant savings year-on-year by enhanced management over vendor spend, which is encouraging the overall ability for claims to become a cost-neutral department for Travelers.

Overall, the firm prides itself on being able to deal with and adapt to whatever claim it is faced with.

“Every business faces unique challenges when filing claims. Our brokers and clients are connected with professionals who have handled similar cases and can guide them through the complexities,” adds O’Neill.

Sedgwick

The firm’s approach to communication is no matter the medium, brokers are provided with instant access to key progress information on claims. This extends across telephone, email, face-to-face, or real-time digital updates.

“At the heart of our broker communications is our Via One portal, a digital platform that reduces the need for status-chasing phone calls. Brokers can access comprehensive claim summaries, real-time updates, and valuable management information – anytime, anywhere,” explains chief client officer, Nicola Dryden.

Nicola DrydenSedgwick

Regular broker-focused newsletters that share timely market insights are also issued which feature case studies and technical background information to further assist brokers.

In addition, Sedgwick hosts broker-client seminars to deliver expert presentations on complex issues such as underinsurance and business interruption.

“A recent example is the mock trial presentation we hosted for over 130 insurer and broker clients,” explains Dryden. “Led by our legal services team, we created a realistic court setting and guided attendees through a typical court hearing for a claim. Specialists from our environmental and forensic teams also delivered presentations on the importance of expert evidence.”

Digital progress is a priority for Sedgwick as customers can upload information easily direct from their smartphones without logging on and using passwords, while over 75% of adjuster visits are now booked online.

Their telephone system even features sentiment analysis, which monitors interactions to identify those who may be vulnerable or require additional support.

Dryden says, “This enables teams to provide tailored responses and proactive interventions where they are most needed, turning potential dissatisfaction into opportunities for exceptional service.”

One in three of their claims leverage AI, enabling customers to electronically notify Sedgwick of losses and be automatically directed to the correct expert. This has doubled routing accuracy, minimised hand-offs and accelerated the handling process.

AI is also set to be incorporated into the Via One portal to deliver report summaries, distilling complex information into key actions and further saving brokers’ time.

Further innovation has been deployed for the firm’s motor scheme clients with the uninsured loss recovery (ULR) scheme.

“In pursuing any ULR claim, we work to secure money back for broker clients’ legal expenses, essentially providing complimentary recovery action,” adds Dryden. “Co-branded with the broker, we do all the work, while they benefit from the added value this provides to their clients.”

Conclusion: Broker expectations continue to redefine performance

-

Claims service has become strategic: Carriers that deliver transparent, responsive experiences retain broker and client loyalty.

-

Broker influence is rising: Leading carriers now treat brokers as core partners and prioritise communication alongside technical handling.

-

Operational gaps create business risk: Slow payments, clunky portals and weak adjustment handling drive switching, unless digital spend yields visible broker-facing gains.

-

Expertise alone is insufficient: Consistent basics, firm accountability and tightly governed TPAs meet in-house standards.

-

Technology pairs with human touch: AI, portals and automated triage cut cycle time while proactive, empathetic communication sustains relationships.

The Top Insurance Claims Carriers in the UK |

5-Star Claims

- Allianz

- Aviva

- AXA Insurance

- QBE Insurance

- Sedgwick International

- Zurich

Insights

-

Richard Talbot‑Jones,

Richard Talbot‑Jones,

MBA, FCII, CMgr FCMI, FRGS

Managing Director

Talbot Jones

Methodology

To select the best claims service providers for 2025, Insurance Business UK sourced feedback from insurance brokers. IB’s research team began by surveying a wide range of brokerages to determine what brokers value in a claim’s service providers. The team also spoke to hundreds of brokers across the country, asking them to rate the claims service providers they had worked with over the past 12 months.

The in-depth information gathered enabled the research team to assign weighted values to each of the criteria being rated by brokers. At the end of the research period, the service providers that received the highest rankings in terms of work quality, specialist expertise and client service were named 5-star award winners in claims insurance.

Keep up with the latest news and events

Join our mailing list, it’s free!