Top Insurance Brokerages and Fastest-Growing Insurance Brokerages in Australia and New Zealand

Jump to winners | Jump to methodology

Strategies combine: people, culture and systems

The top brokerages spanning Australia and New Zealand have transformed headwinds into horsepower.

The winners featured on Insurance Business’ Top Brokerages and Fast Brokerages 2025 lists set the benchmark for the region. The survey celebrates brokerages that excel in performance and growth and shows what is working inside the leading operations.

Top Brokerages are ranked on per-broker results across clients, policies, revenue and growth for the 2024–25 year. Fast Brokerages are those firms recognised for posting more than 20% combined growth in gross written premium and revenue across 2023–24 and 2024–25, backed by clear milestones.

Here is what they’ve achieved (figures represent averages):

Top Brokerages

-

Clients per broker 2025: 338

-

Policies per broker 2025: 674

-

Revenue 2024–25 with broker count: $9,909,332 (31 brokers)

-

Client growth percentage: 37%

Fast Brokerages

-

GWP growth: 40%

-

Revenue growth: 42%

-

Revenue from new policies 2024–25: $1,733,580

-

New clients 2024–25: 1,188

Katherine Wilson, CEO of the Insurance Brokers Association of New Zealand (IBANZ), highlights her key ingredients for growth. “Good customer service and a laser focus on meeting clients’ insurance needs in a way that delivers the best value really stand out in more difficult times,” she explains. “We all know that the insurance landscape is getting increasingly complex to navigate. Brokers play a critical role in providing advice to clients. Those that can truly understand and tailor their client’s insurance needs will stand out above the crowd.”

While fellow industry expert Stephen Jones, head of state management, Australia at HDI, believes an enhanced digital presence enables brokerages to attract new clients with user-friendly websites, intuitive client portals and mobile apps. “Tailored offerings are also another really good way to attract clients with personalised policies using client data and advanced analytics,” he says.

Jones feels that top brokerages have to be client-centric, digitally advanced and agile. He adds, “They will offer personalised, transparent and value-driven services through seamless digital platforms while maintaining the human expertise necessary for complex risk assessments. They will be proactive in adapting to regulatory changes, driving operational efficiency and championing things such as ESG principles. They need to have capacity within their business to seize new opportunities.”

This year’s top-ranked brokerages are turning momentum into muscle, reinforcing the areas that drive long-term impact:

-

Broker teams and talent: Headcount has doubled in some firms, with targeted training, clearer metrics and a stronger culture lifting performance. Many are expanding support teams and renewal departments to keep pace.

-

SME and mid-market portfolios: Strongest growth is in small to medium enterprises and mid-sized corporates, where demand for simple, responsive advice is high. Several firms are refining books to focus on these segments.

-

Specialty and regional niches: Expansion in farm, crop, transport, Māori business and specialty lines such as cyber and PI, often tied to regional footprints and sector-specific expertise.

-

Client service and referrals: Improved systems, streamlined renewals and relationship-driven models are driving retention, word-of-mouth referrals and new business acquisition.

-

Authorised representative networks: Several brokerages are scaling through AR growth, attracting professionals drawn to people-first cultures and robust compliance support.

-

Technology and systems: Overhauls of tech stacks, digital lead generation and automation tools are boosting efficiency and enabling brokers to focus on relationships.

Their challenges are similar to those facing the wider industry, which include scaling quickly, attracting and retaining talent, operating in a cost-pressured market and keeping ahead of regulation and client expectations. What sets them apart is the ability to turn those hurdles into drivers of innovation, culture and client loyalty.

2025 winners’ top challenges

-

Growth and scale: Rapid expansion is testing brokerages’ ability to scale operations without losing culture, service quality or compliance discipline.

-

Talent and retention: Recruiting and keeping skilled professionals remains difficult in an aging industry workforce, with firms investing in training, onboarding and succession to build long-term capacity.

-

Market and economic conditions: Premium pressure, rising claims costs and tougher underwriting are squeezing margins while clients remain price-sensitive and expect competitive solutions.

-

Compliance and client expectations: Evolving regulations and higher compliance demands coincide with clients seeking faster, more personalised service, forcing brokerages to integrate discipline with responsiveness.

The sector’s big tests and the brokerages charting a course

Australia and New Zealand’s brokerages are delivering results in a market defined by cost pressure, regulatory intensity and evolving client demand. Recognition in IB’s Top Brokerages and Fast Brokerages report reflects growth and productivity and also the ability to thrive under conditions that continue to test the wider sector.

Market headwinds

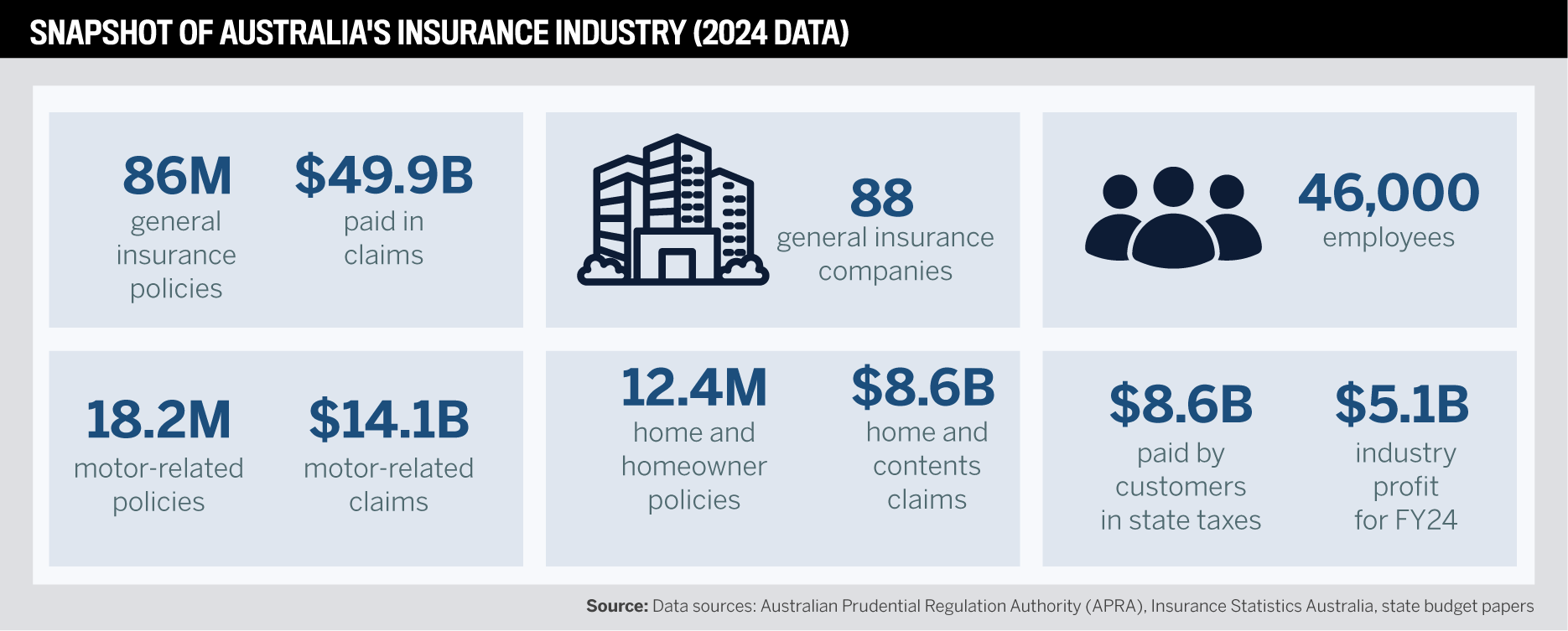

Insurance Council of Australia data show how claims inflation has reshaped the industry.

Inflation, labour and materials

- Building materials cost 30% more than three years ago, with a further 4.3% rise in the 12 months to February 2025.

-

Motor claims rose 42% (2019–24) due to pricier cars, parts, labour and complex technology.

Development in high-risk locations

- A total of 1.4 million properties face flood risk, with ~300K at severe to extreme annual risk, mostly in NSW, Qld and Vic.

-

Since 2022, insurers received ~500K extreme weather claims from the SEQ and northern NSW regions.

Extreme weather costs

- Insured extreme weather costs hit $22.5 billion over 5 years (avg. $4.5 billion/year), up 67% from the previous five years.

-

In 2023, reinsurers raised costs to 20-year highs, with Australian insurers facing increases of up to 30%.

Taxes

- Taxes add 20–40% to insurance premiums, benefiting state governments most.

-

In 2023–24, states collected ~$8.6 billion in insurance taxes, $3.5 billion more than the industry’s total profit.

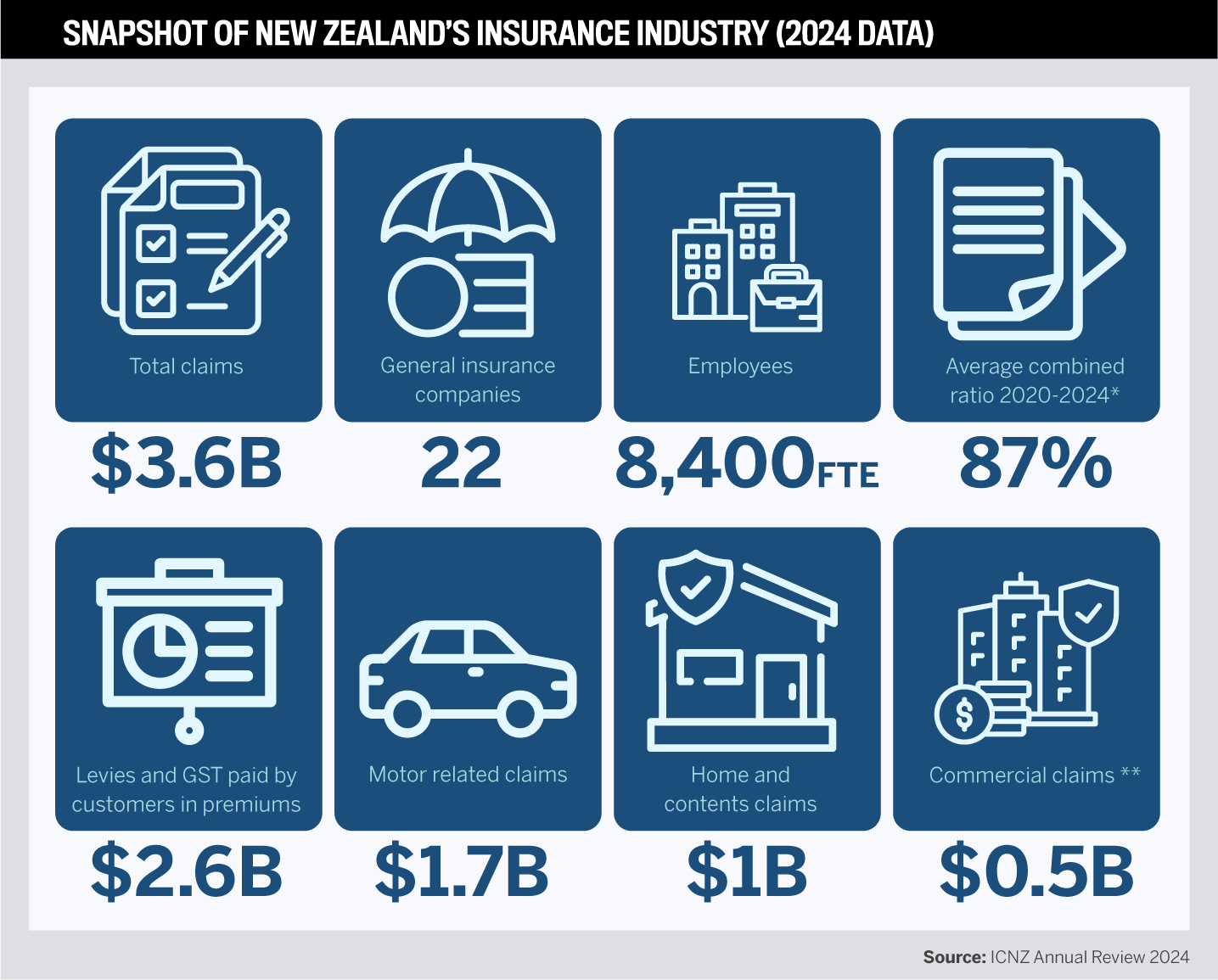

The New Zealand market faces similar pressures, according to the Insurance Council of New Zealand.

Worsening extreme weather

- Natural disasters have caused more than $31.2 billion in insurance claims since 2010, split between earthquakes (80%) and extreme weather events (20%), not including the damage to infrastructure such as roads, rail and electricity and telecommunications networks.

-

Excluding earthquakes, extreme weather has caused over $6 billion in claims since 2010, with over 60% of that because of the Auckland Anniversary Weekend flooding and Cyclone Gabrielle events in early 2023.

Inflation, labour and materials

- Government levies and GST add a further burden, accounting for up to 43% of a household's insurance premium.

-

Construction costs remain elevated, with residential building expenses rising more than 40% since 2019, despite government efforts to open the market to lower-cost imported materials, according to New Zealand government data.

More people in harm’s way

- An estimated 675,500 New Zealanders live in areas already prone to flooding.

-

Over 72,000 Kiwis are potentially affected by rising sea levels in the future.

-

Nearly 50,000 buildings are currently exposed to coastal flooding, and at the highest range of warming scenarios, that could rise to nearly 120,000 this century.

-

Preliminary research shows 125,600 buildings are at risk if the sea level rises 1 metre, at a replacement cost of $38 billion.

Growth to continue

Australia’s general insurance market is set to keep expanding, with gross written premiums on track to reach $144.5 billion by 2029. GlobalData attributes that to an 8.8% compound annual growth rate (CAGR). For brokers, that growth widens the addressable market and raises the bar on execution. Brokerages that convert demand into per-broker productivity, maintain strong compliance and invest in service models are best placed to capture share in a cycle that still tests pricing and claims discipline.

GlobalData also projects similar momentum in New Zealand. The country’s life insurance market is projected to grow from $3.5 billion in 2024 to $4.8 billion by 2029, registering a CAGR of 7.0% in gross written premiums. The growth is driven by higher demand for whole life and personal accident and health insurance, along with increased awareness of protection policies.

The data and analytics firm also expects the market to grow by 8.2% year on year to $3.8 billion in gross written premiums in 2025. This year’s growth rate will be driven by an ageing population, heightened health awareness and the rising cost of living.

Leadership priorities

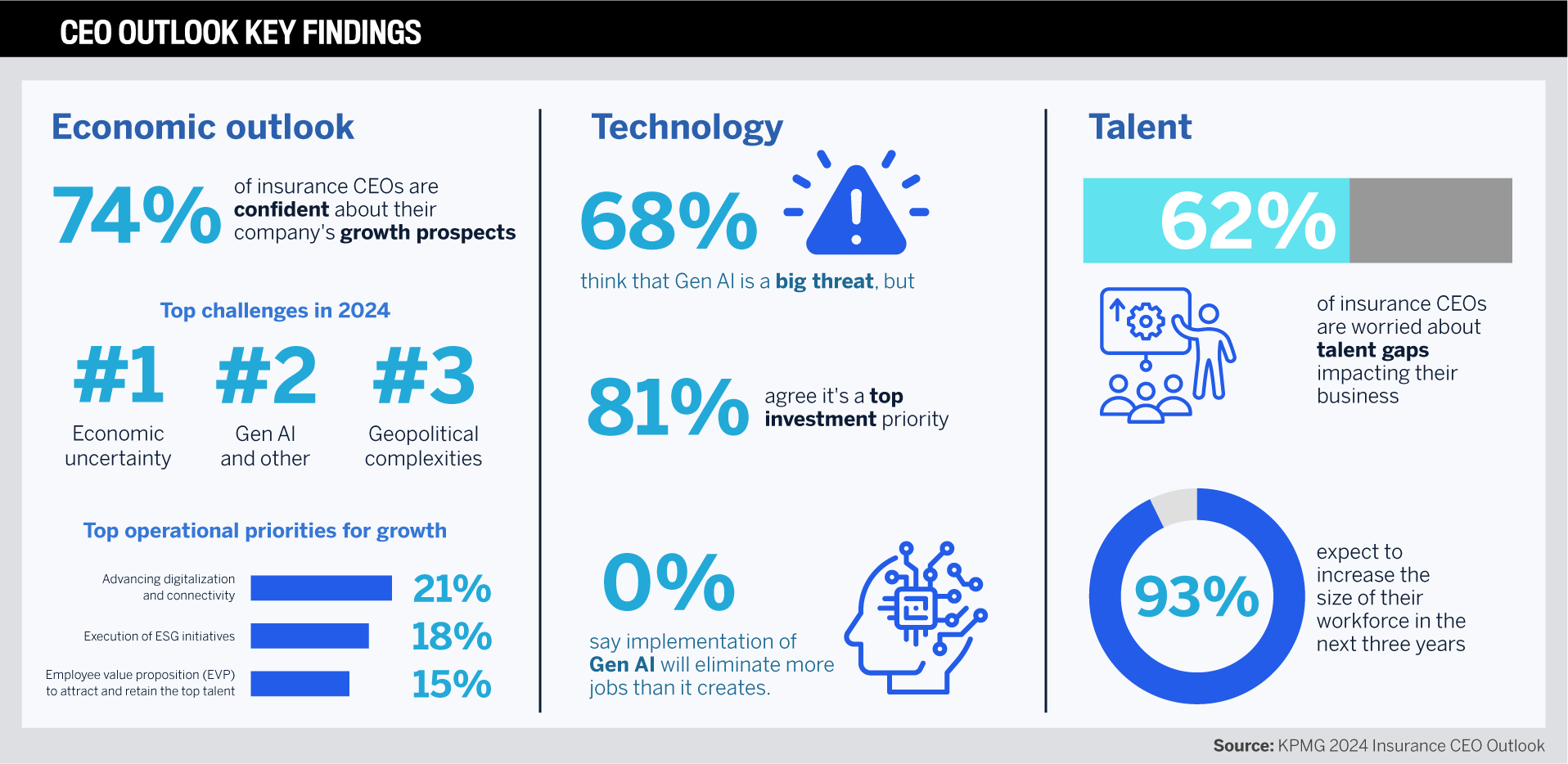

KPMG’s Insurance CEO Outlook highlights how executive agendas align with what the top brokerages are achieving.

Insurance CEOs remain wary about the global outlook, yet most still expect growth. In KPMG’s report, 59% forecast earnings gains above 2.5% over the next three years, and 15% expect more than 5%. Hiring plans are strong, too, with 93% planning to add staff and about one-third aiming for workforce growth of 6% or more.

PwC’s latest Australia insurance outlook points to intensified oversight from APRA and ASIC, rising expectations for pricing transparency, and a push to adopt AI and broader digital tools. The takeaway is steady compliance and tech-enabled execution to sustain trust and growth.

In New Zealand, the Conduct of Financial Institutions regime took effect on 31 March 2025. It requires registered banks, licensed insurers and non-bank deposit takers to run fair conduct programs that embed fair treatment in product design, distribution and complaints handling. Brokerages and other intermediaries face rules on incentives and fair distribution. The framework increases compliance demands and gives advice-led firms a chance to stand out.

For continued growth, Jones states there is a need to build a digital-first backbone to allow brokers the time to build authentic relationships with clients. There is also the digital marketing avenue of using social media, SEO and targeted ads to generate leads.

“Niche specialisation is a really good concept to consider or focus on underserved sectors of the industry or where there might be emerging risks, where there’s a real client thirst or knowledge for understanding how to get ahead of the game,” he says.

Embracing regulation and expanding compliance knowledge is another area that Jones sees as a driver of growth. He adds, “Client relationships will become advisory and less transactional. It will be a significant point of difference as we start to consolidate a number of the functions. The personal client advisory will be far more in demand.”

Client expectations

According to the Vero SME Insurance Index 2025, advice and broker expertise remain among the top reasons SMEs work with brokers (88%), while support during claims and service quality are consistently strong priorities. The report shows that SMEs place a higher value on trusted guidance and relationships than on price alone.

New Zealand insurers are reshaping products and services around what clients want most, including personalised cover, easy digital access and quick, transparent claims, according to Deloitte’s 2025 global trends report. Climate and regulatory pressure are speeding up the shift to smarter tech, stronger data safeguards, and advice clients can trust.

Jones says, “Clients now expect personalised advice, seamless digital experiences, instant access to information and a quick claims process, including instantaneous understanding of where a claim may be in the actual process.”

This year’s award winners show how these trends play out in their markets. Across the list, firms emphasise disciplined growth forged around trust, empowerment and client-first thinking. They invest in systems that free brokers to advise, embed compliance in daily work and develop people with the same intent they bring to revenue.

Shielded Insurance, ranked No. 1, shows how a brokerage can harness technology and structured onboarding to deliver both scale and consistency.

When Joshua Scutts co-founded the Queensland brokerage, he set out to build more than a high-volume brokerage. His vision was to create a business that combined client trust, broker empowerment and modern systems to challenge the way insurance is traditionally delivered.

That formula has propelled Shielded to the very top of IB’s Top Brokerage list while also being named a Fast Brokerage for 2025.

For Scutts, success starts with relationships. “We are high volume, but we don’t just look at transactions; we’re also looking to build long-term relationships with our clients,” he says.

That focus has fuelled retention and referrals while building the kind of reputation that attracts both new customers and brokers.

Building the Shielded engine

Shielded’s growth has been deliberate. The firm invested early in technology to strip away administrative work and free brokers to do what they do best: give advice. Scutts points to the firm’s proprietary systems for quoting, claims tracking, lead management and communication as key differentiators. Together, these tools form what he calls “the Shielded engine”, a platform that supports brokers to succeed and creates consistent client experiences.

The results are tangible. Shielded boasts more than 9,000 five-star reviews online and renewal rates that rank among the strongest in the industry. “Compliance is probably No. 1 on our list,” Scutts says, adding that growth has only strengthened the company’s commitment to rigorous checks and frameworks.

Scaling culture with size

With expansion comes complexity, and Scutts is clear about his role. “As a leader of the business, I know my core role now is people and culture, to make sure that vision of what we want Shielded to be really trickles down to everyone in the business,” he says.

That vision is anchored in challenging the status quo. Shielded recruits and trains brokers through a structured onboarding program that emphasises both technical skills and cultural fit. Standardised processes and compliance checks mean clients receive the same level of service regardless of which broker they work with. This approach creates consistency while preserving the brokerage’s collaborative culture.

Formula for growth

Shielded’s rapid rise is no accident. Scutts has a formula he often repeats: growth equals innovation plus marketing. The brokerage deliberately focuses on underserved markets, particularly small and mid-sized businesses and specialty lines. By coupling targeted positioning with innovative systems, Shielded has built a reputation that attracts top brokers and clients alike.

The firm’s early adoption of technology has been central to that momentum. Brokers joining from other firms are often “blown away” with the way the team operates and the systems in play. That reputation has made recruitment easier, fuelling expansion without sacrificing culture.

Balancing speed and discipline

For Scutts, balancing growth with quality is a priority. Shielded builds systems that scale, refining processes as volumes increase. AI tools are deployed as copilots for brokers, helping them deliver advice with speed and accuracy. Feedback loops from clients and brokers ensure the company responds quickly when issues arise.

“It’s not anything like quality over quantity; it’s quality and quantity for us,” Scutts explains. His approach is to treat every challenge as a chance to improve, making sure the same problems don’t repeat.

Love for the business

Beyond the metrics and systems, Scutts credits passion as a driving force. “I don’t think you would talk to anyone else who loves their business and loves the industry as much as I do,” he says. That enthusiasm, combined with a disciplined growth strategy and an unshakable client focus, has positioned Shielded as one of Australia’s standout brokerages and a name to watch in the years ahead.

Fundagroup Insurance Brokers in New Zealand demonstrates how even a smaller team can leverage innovation, equity participation and shared ownership to achieve rapid growth.

The No. 12-ranked brokerage is carving out its own path in New Zealand’s competitive insurance market. Under the leadership of CEO Payal Sharma, the firm was also named a Fast Brokerage for 2025. The recognition reflects a strategy centred on trust, innovation and a people-first culture.

Sharma points to performance across multiple measures as the product of deliberate choices. Growth, she says, starts with the first client interaction. Competitive quoting, risk insights and clear comparisons set the stage for trust and conversion.

“Our sustained performance across key metrics, including client growth, broker productivity, and revenue, comes down to a few core principles. First, we’ve built a culture of trust and transparency that resonates with both our clients and our team.

“Second, we invest heavily in training and technology, ensuring our brokers are not just well-informed but empowered to deliver exceptional service to negotiate the closing. And third, we stay agile, adapting quickly to market shifts while keeping our clients’ long-term goals at the centre of every decision.”

Building consistency at scale

Sharma is quick to emphasise that culture and service cannot be diluted as the brokerage expands. Fundagroup has anchored its growth in values such as integrity, responsiveness, and client-first thinking, embedding them directly into systems and compliance programs.

She believes the firm’s strength comes from the sense of shared ownership that unites the team. “We grow together because our culture is built on shared ownership, multitasking excellence and a client-first philosophy. Every success is collective, every challenge is met with agility and every client is served with consistency and care.”

Equity participation for key team members reinforces that sense of belonging. The model turns brokers into long-term contributors rather than short-term hires. Sharma calls this an emotional investment that keeps people motivated and accountable while creating stability for clients.

Momentum through innovation

Fundagroup’s rapid growth has been fuelled by leaning into the Steadfast Broker Network portals, intuitive digital platforms and the strategic use of AI bots to streamline operations. Parametric risk solutions are another area of experimentation, adding new dimensions to client service.

“Our momentum is rooted in innovation that fills the gaps traditional insurance leaves behind,” Sharma says. With a team of five full-time brokers whose backgrounds span risk engineering, loss adjustment, underwriting and international markets, the firm experiments boldly with management techniques and value propositions. Some ideas succeed, others don’t, but each client interaction becomes a chance to adapt and refine.

Growth with discipline

Balancing speed with quality is one of Sharma’s ongoing priorities. She acknowledges the natural uplift in growth that comes from premiums, levies and inflation but insists that engineered growth must be managed differently. Fundagroup invests in people as much as systems, offering continuous learning, equity pathways, and a strong culture of ownership.

Community engagement is also part of the equation. The brokerage supports local sports and events, strengthening personal connections beyond digital touchpoints. Referrals and client diversification often follow positive claim outcomes, making growth organic as clients become advocates.

Sharma frames it all as a long-term mission. “We’re not just building a business; we’re building a unique succession plan model, having a legacy of ethical, empowered brokers who serve with integrity and stay in the industry for life,” she says.

Conclusions: how Top Brokerages are building the next model of growth

-

The Top Brokerages and Fast Brokerages of 2025 prove that scale and service are complementary drivers of success.

-

Their growth stories show that talent pipelines, client trust and disciplined systems are now as critical to competitiveness as premium volumes.

-

What emerges is a sector where resilience is measured by the ability to adapt culture, technology and compliance into everyday practice.

-

For insurers, partners and clients, the takeaway is that the brokerages leading today are building business models that can withstand volatility while still strengthening relationships.

Top Insurance Brokerages and Fastest-Growing Insurance Brokerages in Australia and New Zealand

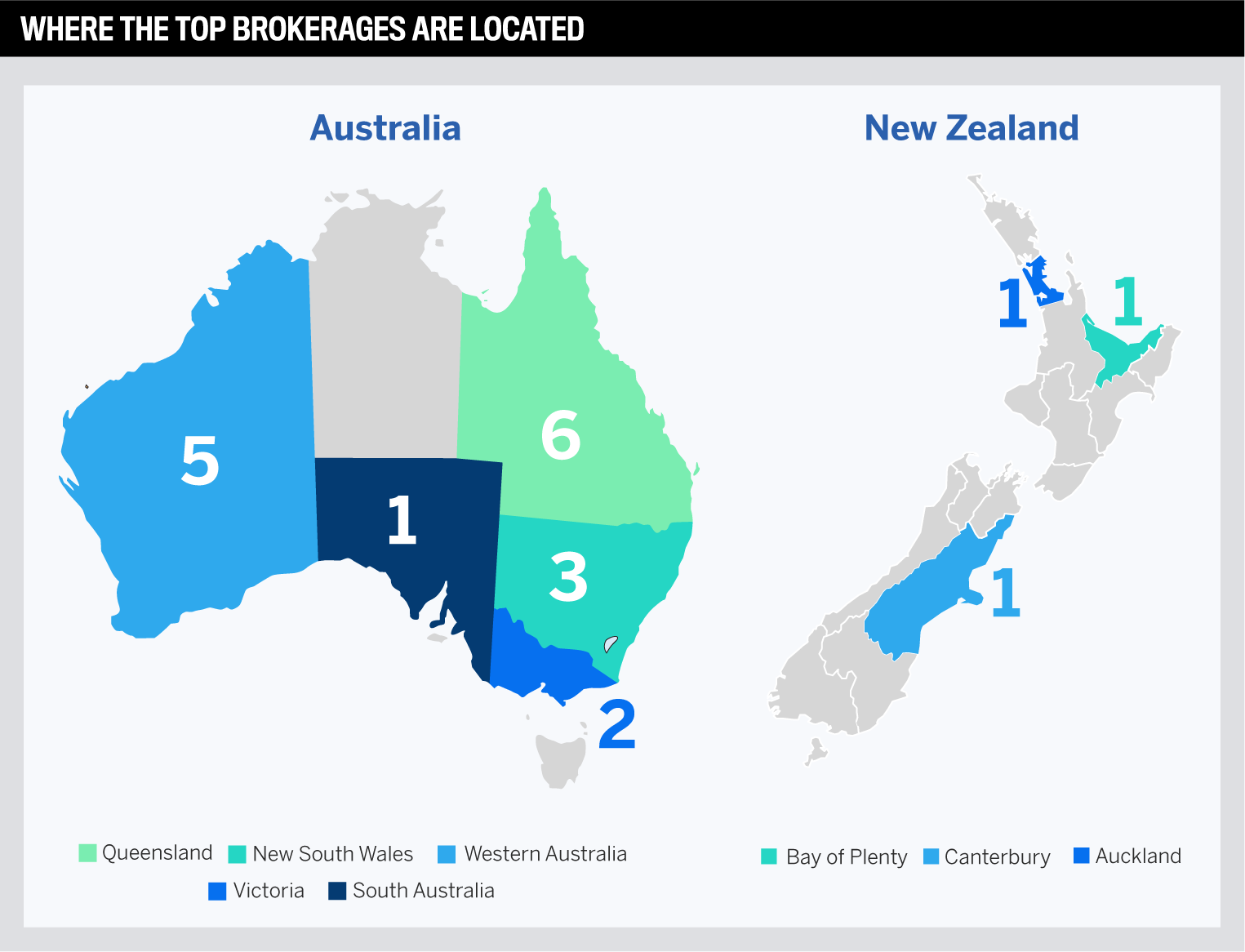

Top Brokerages by rank

- 2. Stonewell Insurance Brokers

- 8. O’Connor Warren Insurance Brokers

- 9. Aviso WA Insurance Brokers

- 10. Grace Insurance

- 11. Gerrards

- 14. Guardian Insurance Brokers

- 15. Strata Insurance Solutions

- 16. Fortuna Insurance Services

- 17. Elliott Insurance The Green Broker

- 18. Delmont Insurance Group

- 19. Clear Insurance

- 20. McLardy McShane

Fast Brokerages

- Aviso WA Insurance Brokers

- Delmont Insurance Group

- Fortuna Insurance Services

- Gerrards

- McLardy McShane

- Stonewell Insurance Brokers

- Strata Insurance Solutions

Insights

Methodology

The Top Brokerages and Fast Brokerages reports by Insurance Business serve as authoritative benchmarks in the ANZ insurance landscape. These comprehensive analyses not only spotlight the industry's leading performers but also provide invaluable insights into the operational and growth dynamics of brokerages. By meticulously evaluating key performance indicators and growth trajectories, these reports offer a nuanced understanding of the factors driving success in the sector.

Top Brokerages

Brokerages with three or more brokers, headquartered in Australia and New Zealand, submitted data for the 2024/25 financial year. Rankings were based on multiple criteria, including client numbers, policy volumes, revenue and growth metrics, all evaluated on a per-broker basis. Brokerages were scored across these criteria, with the lowest cumulative score determining the top ranking.

Fast Brokerages

Submissions for the 2025 Fast Brokerages awards focus on brokerages demonstrating significant growth. Revenue data for 2023/24 and 2024/25 financial years, alongside growth milestones, were assessed. Brokerages achieving over 20% combined growth in gross written premium and revenue were recognised.

Keep up with the latest news and events

Join our mailing list, it’s free!